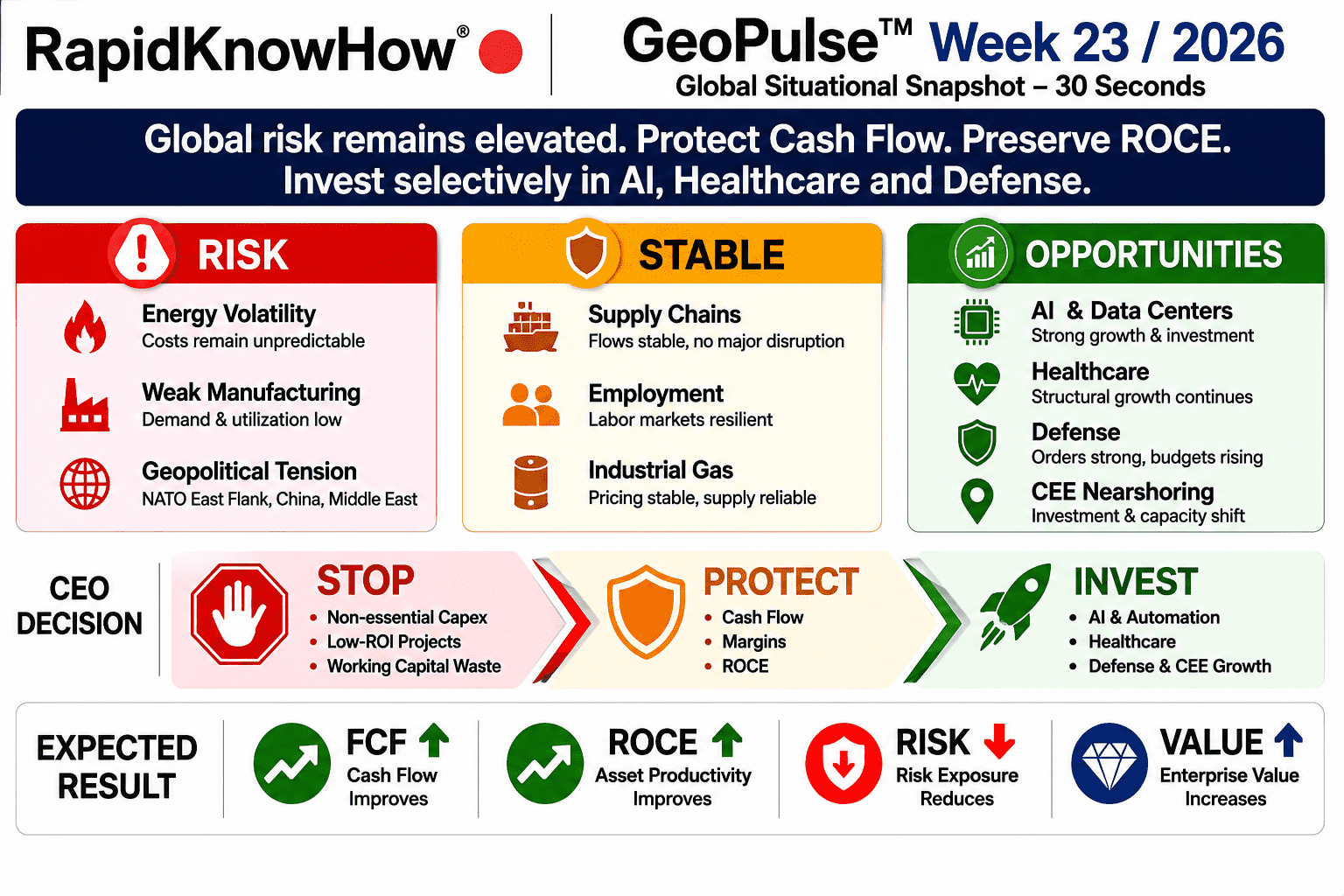

GLOBAL SITUATIONAL SNAPSHOT – EXECUTIVE DASHBOARD

WEEK 23 / 2026 FORECAST

Business • Geopolitics • Life

Europe • DACH • CEE Focus

A) EXECUTIVE SUMMARY (30 Seconds)

GLOBAL STATUS

🟠 CAUTION

The world economy remains stable but fragile.

Three dominant forces continue shaping the environment:

- Geopolitical fragmentation

- Industrial competitiveness pressure

- AI-driven capital reallocation

For CEOs and investors, the key theme remains:

Protect Cash Flow → Preserve ROCE → Invest Selectively

B) EISENHOWER EXECUTIVE MATRIX

| Priority | Topic | Impact | Action |

|---|---|---|---|

| 🔴 DO NOW | Energy Cost Volatility | Very High | Protect margins |

| 🔴 DO NOW | Supply Chain Resilience | Very High | Dual sourcing |

| 🔴 DO NOW | AI Productivity Gap | Very High | Accelerate AI adoption |

| 🟠 SCHEDULE | Manufacturing Optimization | High | Improve utilization |

| 🟠 SCHEDULE | Workforce Upskilling | High | AI competencies |

| 🟡 DELEGATE | Administrative Digitization | Medium | Automate |

| 🟢 MONITOR | Consumer Confidence | Medium | Watch |

C) WHAT CHANGED SINCE LAST WEEK?

↑ Increased

Geopolitical Risk

- NATO eastern flank remains sensitive.

- Black Sea logistics risk remains elevated.

Industrial Competition

- European competitiveness concerns intensified.

- Pressure from US and Asian manufacturing continues.

AI Investment

- Capital continues shifting toward AI infrastructure.

↓ Improved

Energy Supply

- No major disruption observed.

- Storage levels remain supportive.

Supply Chain

- Container flows remain stable.

- Freight bottlenecks limited.

↔ Unchanged

Europe

- Weak growth.

- High energy costs.

- Manufacturing pressure.

D) GLOBAL BUSINESS HEATMAP

| Sector | Status | Trend |

|---|---|---|

| Defense | 🟢 Strong | Up |

| AI Infrastructure | 🟢 Strong | Up |

| Data Centers | 🟢 Strong | Up |

| Healthcare | 🟢 Strong | Up |

| Logistics | 🟠 Stable | Flat |

| Industrial Gas | 🟠 Stable | Flat |

| Automotive | 🟠 Weak | Flat |

| Chemicals | 🔴 Weak | Down |

| Steel | 🔴 Weak | Down |

E) EUROPE / DACH / CEE FOCUS

🇩🇪 Germany

Status

🔴 Weak

Issues:

- Automotive pressure

- Chemical industry weakness

- High energy costs

Outlook

Weak stabilization.

🇦🇹 Austria

Status

🟠 Stable

Strengths:

- Services

- Tourism

- Specialized manufacturing

Risk:

- German slowdown

🇨🇭 Switzerland

Status

🟢 Strong

Strengths:

- Healthcare

- Pharma

- Financial Services

🇵🇱 Poland

Status

🟢 Strong

Benefiting from:

- Nearshoring

- Logistics

- Defense investments

🇨🇿 Czech Republic

Status

🟠 Stable

Dependent on:

- German industrial demand

🇸🇰 Slovakia

Status

🟠 Stable

Risk:

- Automotive exposure

🇭🇺 Hungary

Status

🟠 Stable

Risk:

- Energy dependence

F) NET CASH-FLOW IMPACT LENS

ENERGY

0–30 Days

| Factor | Impact |

|---|---|

| Electricity | 🔴 Negative |

| Gas | 🟠 Neutral |

| Oil | 🟠 Neutral |

Actions

✓ Hedge exposure

✓ Improve efficiency

RED FLAG

🚨 TTF Gas +25% combined with Brent >105 USD

Expected effect:

- FCF deterioration

- Margin pressure

- ROCE decline

SUPPLY CHAIN

0–30 Days

| Factor | Impact |

|---|---|

| Freight | 🟢 Positive |

| Ports | 🟢 Stable |

| Inventory | 🟠 Neutral |

Actions

✓ Dual sourcing

✓ CEE supplier development

MANUFACTURING

0–30 Days

| Factor | Impact |

|---|---|

| Capacity Utilization | 🔴 Negative |

| Labor Cost | 🟠 Neutral |

| Automation | 🟢 Positive |

Actions

✓ Improve utilization

✓ Reduce working capital

✓ Focus on productivity

G) ROCE DELTA ESTIMATOR

| Sector | Expected ROCE Impact |

|---|---|

| AI Infrastructure | 🔺 +2% to +5% |

| Defense | 🔺 +1% to +3% |

| Healthcare | 🔺 +1% to +2% |

| Logistics | ↔ 0% to +1% |

| Industrial Gas | ↔ 0% to -2% |

| Automotive | 🔻 -1% to -3% |

| Chemicals | 🔻 -2% to -4% |

H) INDUSTRIAL GAS (IGAS) DEEP DIVE

Pricing

Current Situation

🟠 Stable

Large suppliers continue disciplined pricing.

No major price war visible.

Energy Input Costs

| Item | Status |

|---|---|

| Electricity | 🔴 Elevated |

| Natural Gas | 🟠 Moderate |

| Diesel | 🟠 Moderate |

Implication

Energy remains the biggest margin lever.

Supply Reliability

Status

🟢 Good

No major shortage signals.

Customer Demand

Strong

🟢 Healthcare

🟢 Electronics

🟢 Food & Beverage

🟢 Data Centers

Weak

🔴 Chemicals

🔴 Steel

🔴 Heavy Industry

Margin Outlook

0–30 Days

🟠 Stable

30–90 Days

🟢 Slight Improvement

If energy costs remain under control.

I) IGAS CEO PLAYBOOK

Priority 1

Protect Energy Margin

Priority 2

Increase Contract Indexation

Priority 3

Focus on Growth Segments

✓ Healthcare

✓ Electronics

✓ Data Centers

✓ Defense

Priority 4

Reduce Working Capital

✓ Cylinder utilization

✓ Fleet utilization

✓ Inventory reduction

Priority 5

Improve ROCE

Target:

ROCE > 20%

through asset productivity rather than volume growth.

J) LIFE DASHBOARD

| Indicator | Status |

|---|---|

| Employment | 🟢 Stable |

| Inflation | 🟠 Moderate |

| Housing | 🟠 Weak |

| Travel | 🟢 Strong |

| Healthcare | 🟢 Strong |

| AI Impact on Jobs | 🔺 Accelerating |

K) TOP 5 OPPORTUNITIES (NEXT 90 DAYS)

- AI Productivity Programs

- Defense Supply Chains

- Data Center Expansion

- Healthcare Investments

- Nearshoring into CEE

L) TOP 5 RISKS (NEXT 90 DAYS)

- Energy Cost Shock

- Geopolitical Escalation

- Manufacturing Weakness

- Chemical Sector Recession

- Delayed AI Adoption

M) RAPIDKNOWHOW CEO CONCLUSION

Global Risk Level

🟠 Elevated but Manageable

Europe Outlook

🟠 Weak but Stabilizing

DACH Outlook

🟠 Cautious

CEE Outlook

🟢 More Attractive than Western Europe

Industrial Gas Outlook

🟠 Stable with Selective Growth Opportunities

CEO Action for Week 23

Protect Cash Flow → Improve Asset Productivity → Preserve ROCE → Invest Selectively in AI, Healthcare, Defense and Data Centers.

RapidKnowHow® GeoPulse™ Week 23 / 2026

Mastering Global Opportunities with GeoPower Intelligence 🔴