A) POWER REPORT: Leader / Laggard / Loser – Industrial Gas Sector 2026–2030

The industrial gas sector from 2026 to 2030 will not be won by the biggest producers alone. It will be won by the companies that convert gas supply into cash-flow resilience, customer lock-in, asset productivity, energy-risk control, digital replenishment, and AI-orchestrated value capture.

The sector remains structurally attractive: demand is supported by healthcare, electronics, food, chemicals, metal fabrication, energy transition, hydrogen, carbon capture, and resilient local distribution.

Market forecasts point to mid-single-digit growth: one 2026 forecast expects the global industrial gases market to grow from about USD 122 billion in 2026 to USD 194 billion by 2036, while another projects growth to about USD 126.5 billion by 2030 from USD 98.8 billion in 2025. Europe is also expected to grow around 4.7% CAGR from 2026–2030, supported by green hydrogen and industrial transformation.

But growth alone will not separate winners from losers.

The decisive question is: Who converts growth into FCF, ROCE, valuation multiples, compounded growth, and market value?

B) The Three Strategic Positions

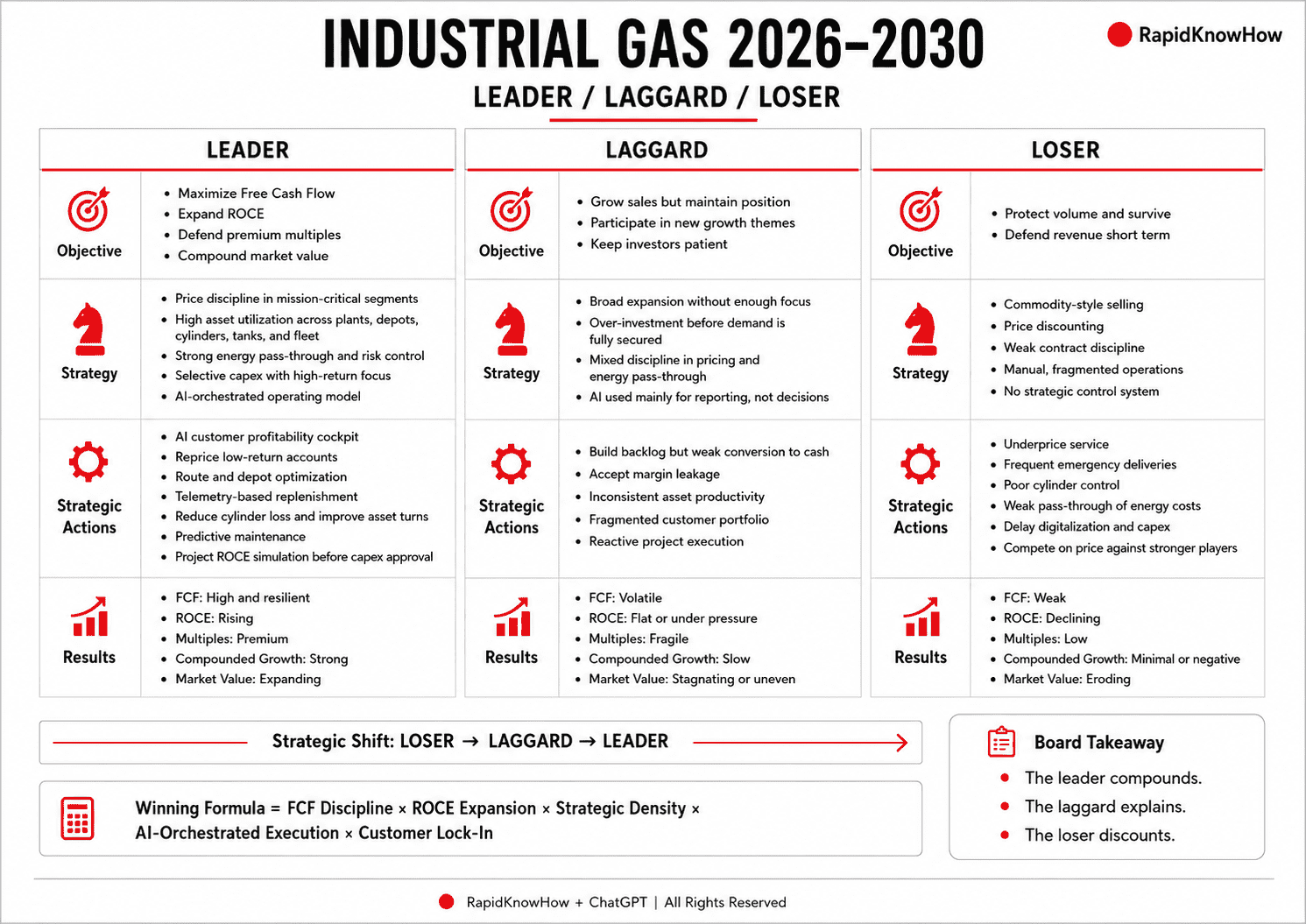

1. The Leader: AI-Orchestrated Cash-Flow Compounder

The industrial gas leader of 2026–2030 will not simply sell oxygen, nitrogen, argon, hydrogen, helium, CO₂, or specialty gases. The leader will operate a strategic gas operating system.

The leader’s objective is clear: maximize Free Cash Flow first, improve ROCE second, defend premium multiples third, and compound market value over time.

This leader will focus on five strategic priorities:

First, protect pricing power. Industrial gases have local density economics. The best players defend price through reliability, safety, service quality, long-term contracts, and mission-critical applications. They avoid commodity discounting.

Second, raise asset utilization. Cylinders, tanks, trailers, ASUs, hydrogen plants, depots, and distribution fleets must be orchestrated as one system. Idle assets destroy ROCE. Optimized replenishment improves FCF.

Third, pass through energy cost volatility. Energy is a major input in gas production. Leaders build strong pass-through clauses, hedging logic, and customer segmentation models. They do not absorb volatility silently.

Fourth, invest only in risk-adjusted high-return projects. Large hydrogen, ammonia, carbon capture, and electronics projects can create long-term growth, but they can also destroy value when capital is committed before demand, regulation, or offtake economics are secure.

Fifth, use AI as a margin engine, not as a slogan. AI must drive route optimization, cylinder visibility, predictive maintenance, demand forecasting, customer profitability, depot productivity, energy management, and contract discipline.

Linde currently shows many leader characteristics. In 2025, it generated USD 10.4 billion operating cash flow, invested USD 5.3 billion in capex, returned USD 7.4 billion to shareholders, and reported an adjusted operating profit margin of 29.8%.

In Q1 2026, Linde reported sales of USD 8.8 billion, adjusted operating margin of 30.0%, operating cash flow of USD 2.24 billion, and guided to 7%–9% adjusted EPS growth for 2026. Its current market capitalization is about USD 230 billion, with a P/E ratio around 32.7, showing that the market pays a premium for visible compounding quality.

Air Liquide also shows strong leader characteristics, especially in transformation discipline. In 2025 it reported operating margin above 20%, cash flow from operating activities before working-capital changes above EUR 6.8 billion, recurring ROCE of 11.2%, and a new margin objective of another +100 basis points in 2027. Its market capitalization is around EUR 101–102 billion, with P/E estimates in the high-20s, depending on source and listing.

Leader result 2026–2030:

Higher FCF, stable or rising ROCE, premium valuation multiple, lower cost of capital, stronger acquisition capacity, and compounding market value.

2. The Laggard: Growth Without Cash Discipline

The laggard is not necessarily a bad company. The laggard may still grow sales, announce large projects, and participate in hydrogen, electronics, healthcare, and energy transition. But the laggard fails to convert activity into superior cash flow and ROCE.

The laggard’s objective is usually too broad: grow everywhere, defend all positions, enter every new energy theme, and keep investors patient. That creates strategic dilution.

Typical laggard strategies include:

Over-investing before demand is secured. Large clean hydrogen or ammonia projects can be attractive, but only when offtake, subsidies, regulation, financing, and execution risk are controlled.

Confusing backlog with value creation. A big project backlog is not automatically good. It becomes valuable only when it converts into predictable cash flow at attractive returns.

Running regional businesses without enough local density. Industrial gases reward route density and customer concentration. Weak density increases delivery cost and reduces margin.

Accepting margin leakage. Poor cylinder control, weak rental discipline, unmanaged energy pass-through, fragmented pricing, and underpriced emergency service destroy hidden value.

Using AI as reporting technology, not operating technology. Dashboards alone do not improve ROCE. AI must change decisions, timing, pricing, routing, replenishment, maintenance, and customer selection.

Air Products is an example of a company with high-quality industrial gas assets but visible transition and execution risk. Its fiscal 2025 report describes regional gases across Americas, Asia, Europe, and Middle East/India, while investor materials highlight priorities such as traditional industrial gas backlog execution, NEOM green hydrogen, CCS/ammonia derisking, and disciplined capital deployment.

At the same time, the company reported fiscal 2025 GAAP results including a loss per share and operating loss, making capital discipline and project derisking central issues for the 2026–2030 period. Its market capitalization is currently about USD 65.8 billion, with a P/E around 31.2.

Laggard result 2026–2030:

Sales may grow, but FCF remains volatile. ROCE stagnates or falls. Multiples become fragile. Market value compounds slowly or becomes dependent on restructuring, portfolio simplification, or activist pressure.

3. The Loser: Commodity Gas Seller Without Strategic Control

The loser in the industrial gas sector is the player who stays trapped in the old model: produce gas, deliver gas, invoice gas, repeat.

This player has no strategic control system. It does not know its true customer profitability. It underprices service. It loses cylinders. It delivers too often. It has weak contract discipline. It suffers from energy volatility. It cannot defend margins. It reacts to customer demand instead of orchestrating it.

The loser’s objective is survival: maintain volume, keep customers, fill trucks, and protect short-term revenue. But this destroys long-term value.

The loser strategy is defensive and fragmented:

Price to keep volume. This protects revenue but destroys margin.

Delay investment. This protects short-term cash but creates reliability and safety risk.

Accept operational complexity. Too many small customers, emergency deliveries, poor planning, and manual processes create hidden cost.

Ignore digital replenishment. Without telemetry, AI scheduling, and customer-level profitability, the business becomes blind.

Compete against leaders on price. This is the fastest route to value destruction.

The loser may still exist in 2030, but as an acquisition target, regional niche player, or low-return distributor. Its market value will not be determined by strategic growth, but by replacement value, local customer lists, depot access, or consolidation potential.

Loser result 2026–2030:

Weak FCF, declining ROCE, low valuation multiple, limited reinvestment capacity, and no compounding growth.

C) RapidKnowHow Strategic Action System 2026–2030

The winning formula is:

Industrial Gas Value = FCF Discipline × ROCE Expansion × Strategic Density × AI-Orchestrated Execution × Trust-Based Customer Lock-In

The sector leader must execute ten moves:

- Build an AI customer-profitability cockpit.

- Rank every customer by FCF, ROCE, service intensity, and strategic value.

- Reprice low-return accounts.

- Install energy pass-through discipline.

- Optimize route density and depot productivity.

- Automate replenishment with telemetry and demand forecasting.

- Reduce cylinder loss and improve asset turns.

- Separate high-return base gas from high-risk mega-project capital.

- Use AI to simulate project ROCE before committing capital.

- Communicate FCF, ROCE, and market-value impact clearly to investors.

Final Board Insight:

From 2026 to 2030, industrial gas leaders will not be those who chase the most fashionable growth story. They will be those who convert every molecule, cylinder, tank, route, contract, customer, and project into measurable cash-flow power. The leader compounds. The laggard explains. The loser discounts.- Josef David