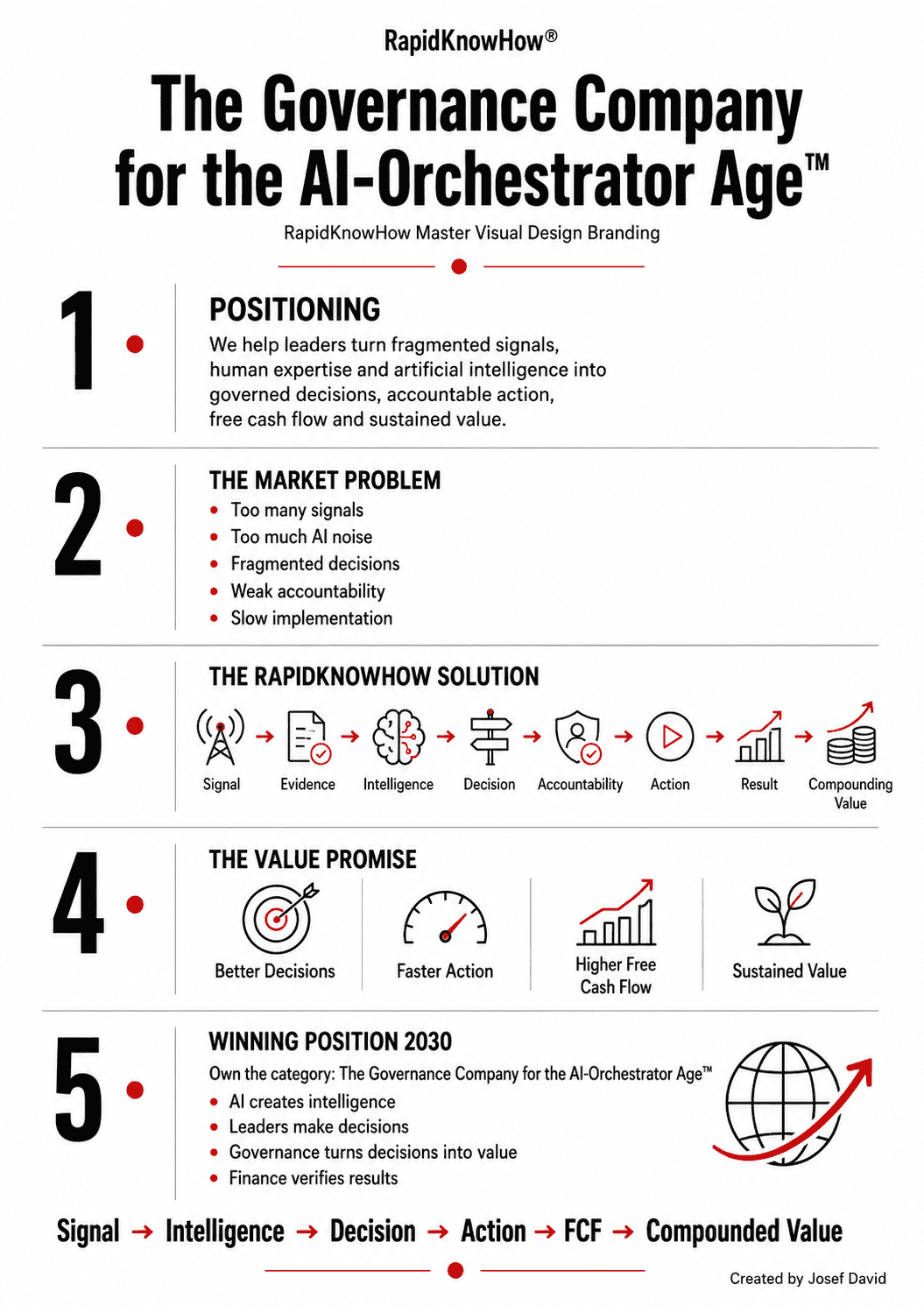

Transforming Industrial-Gas Assets, Customer Relationships and Regional Know-How into Compounding Free Cash Flow

RapidKnowHow® Strategic PowerReport

Created by Josef David

Status: 14 July 2026

Executive Decision

Messer already possesses many of the assets required to become the leading industrial-gas AI-Orchestrator in DACH and Central and Eastern Europe:

- a strong privately controlled industrial-gas platform;

- established companies across Germany, Austria, Switzerland and much of CEE;

- production, filling and distribution infrastructure;

- industrial, medical, electronic and specialty-gas capabilities;

- close regional customer relationships;

- hydrogen and carbon-management know-how;

- a resilient local-for-local operating model;

- family ownership combined with institutional capital;

- sufficient scale to invest, but greater potential agility than the largest listed competitors.

The strategic opportunity is not to imitate Linde or Air Liquide.

It is to create a distinctive leadership position:

Messer becomes the fastest, most regionally connected and most decision-intelligent industrial-gas company in DACH/CEE.

The transformation should move Messer from:

Producing and delivering gases

to:

Orchestrating energy, gases, assets, customer decarbonisation, capital and regional intelligence as one integrated value-creation system.

1. Messer’s Starting Position in 2026

Messer reported 2025 revenue of €4.5 billion, EBITDA of €1.4 billion, an EBITDA margin of 31%, investments of €747 million, more than 12,000 employees, and net debt of €3.2 billion, down €304 million year over year. Messer described its cash flow as strong.

The company attributes part of its resilience to a diversified business model and a local-for-local operating framework. European revenue growth in 2025 was supported particularly by food and beverage and healthcare demand.

Strategic interpretation

Messer is not a turnaround case.

It is a strong industrial company facing a next-level orchestration opportunity.

The question is not:

Can Messer survive?

The question is:

Can Messer use its regional position, private ownership, customer proximity and digital intelligence to create a structurally superior DACH/CEE business model?

2. Why DACH/CEE Is Messer’s Natural Leadership Region

Messer maintains operating companies across Germany, Austria and Switzerland and has a broad presence in CEE and Southeast Europe, including Poland, Czechia, Slovakia, Hungary, Slovenia, Croatia, Romania, Bulgaria, Serbia, Bosnia and Herzegovina, North Macedonia and Ukraine.

This provides a powerful geographic platform connecting:

- Europe’s largest industrial economy;

- energy-intensive manufacturing;

- automotive and machinery corridors;

- steel, metals and chemicals;

- healthcare systems;

- food and beverage production;

- electronics and advanced manufacturing;

- lower-cost and developing CEE locations;

- EU-funded industrial modernisation;

- emerging hydrogen and decarbonisation projects.

In 2023, Messer reported European sales of approximately €1.284 billion. Central Europe sales increased by 22.8%, while Southeast Europe sales increased by 18.8%. Investments included CO₂ facilities in Austria, Czechia, Poland and Serbia, an air-separation plant in Serbia and a filling facility in Romania.

RapidKnowHow assessment

Messer already owns many of the pieces.

The missing competitive advantage is a visible system that connects them into one regional intelligence and value-creation platform.

3. The Strategic Gap

A traditional industrial-gas company is generally organised around:

- countries;

- product lines;

- production plants;

- sales organisations;

- engineering;

- finance;

- logistics;

- individual investment projects.

This structure creates accountability, but it can also produce fragmentation.

Important information may remain separated across:

- energy procurement;

- plant operations;

- contract management;

- commercial pricing;

- customer demand;

- logistics;

- sustainability;

- capital expenditure;

- political and regulatory intelligence.

The consequence

A company can possess extensive information but still make decisions too slowly.

Examples include:

- delayed energy pass-through;

- inconsistent regional pricing;

- surplus production in one location while another location purchases externally;

- logistics decisions disconnected from energy economics;

- maintenance priorities that ignore customer margin;

- hydrogen projects pursued before bankable demand is secured;

- capital allocated country by country rather than across the highest-value regional opportunities.

The AI-Orchestrator model closes this gap.

4. The 2030 Leadership Position

Messer DACH/CEE AI-Orchestrator Leader 2030™

By 2030, Messer should operate DACH/CEE as an integrated decision ecosystem.

The system continuously connects:

Market Signals

Customer demand, competitor moves, industrial investment and macroeconomic changes.

Energy Signals

Electricity prices, gas prices, grid constraints, renewable availability and procurement contracts.

Asset Signals

Plant capacity, reliability, energy efficiency, maintenance and network utilisation.

Commercial Signals

Pricing, pass-through, contract profitability, churn risk and share-of-wallet.

Customer Signals

Production plans, decarbonisation targets, investment projects and credit exposure.

Regulatory Signals

State aid, carbon pricing, hydrogen rules, medical-gas requirements and competition policy.

Capital Signals

ROCE, free cash flow, net debt, investment pipeline and acquisition opportunities.

The system converts these signals into:

Decision → Action → Measured Result

5. The AI-Orchestrator Is Not an AI Replacement Programme

The model does not replace experienced industrial-gas leaders.

It strengthens them.

Human leaders contribute:

- industrial judgement;

- customer trust;

- safety responsibility;

- negotiation;

- political understanding;

- strategic accountability;

- final decisions.

AI contributes:

- signal detection;

- pattern recognition;

- scenario analysis;

- cross-country comparison;

- anomaly identification;

- decision preparation;

- rapid dashboards;

- implementation tracking.

The AI-Orchestrator leader:

- defines the strategic question;

- validates the relevant data;

- challenges the AI assessment;

- considers commercial and human consequences;

- makes the decision;

- assigns action;

- verifies the result.

The leader remains accountable. AI increases decision speed, range and consistency.

6. The Six Value-Creation Engines

Engine 1 — Energy Orchestration™

Industrial-gas economics depend heavily on electricity.

Messer should combine:

- electricity procurement;

- plant operating schedules;

- renewable-power contracts;

- spot and forward-price signals;

- grid constraints;

- customer demand;

- pass-through recovery

in one regional Energy Decision System.

Decisions

- Which plant should produce?

- When should it produce?

- Which production should be shifted?

- Where should liquid products be sourced?

- Which contracts require repricing?

- Where should renewable electricity be secured?

- Which assets require efficiency investment?

Result

- lower specific energy cost;

- reduced margin volatility;

- faster response to energy shocks;

- improved production-network utilisation;

- stronger free cash flow.

Engine 2 — Commercial and Pass-Through Excellence™

Every major contract should be visible through a common economic lens.

The system should monitor:

- contract margin;

- electricity and fuel pass-through;

- indexation delays;

- minimum purchase obligations;

- transport surcharges;

- customer credit;

- renewal dates;

- competitive exposure;

- strategic customer value.

Red alerts

- negative or declining contribution;

- unrecovered energy costs;

- excessive working capital;

- high service cost;

- repeated emergency deliveries;

- contracts approaching renewal without action;

- customers receiving inconsistent regional terms.

Result

- fewer value-destructive contracts;

- faster price recovery;

- disciplined customer selection;

- improved EBITDA quality;

- stronger cash conversion.

Engine 3 — DACH/CEE Network Optimisation™

Messer’s geographic presence should become an integrated regional advantage.

The system should connect:

- air-separation units;

- CO₂ sources;

- cylinder-filling plants;

- storage;

- distribution;

- cross-border supply;

- external purchases;

- customer clusters;

- logistics routes.

Objective

Supply every customer from the economically and operationally strongest available source—not automatically from the historic country source.

Result

- higher asset utilisation;

- lower external purchasing;

- reduced logistics kilometres;

- better emergency resilience;

- improved regional supply security;

- stronger return on invested capital.

Engine 4 — Customer Decarbonisation Orchestration™

Messer is already developing solutions involving clean hydrogen, oxy-fuel combustion, wastewater applications and carbon management. In 2025, it continued investing in renewable electricity, advanced compressor and control systems, hydrogen and customer-efficiency solutions.

Messer has also introduced ZeCarb, described as a carbon-capture-as-a-service offering for emissions-intensive industries.

These solutions should be integrated into a single customer proposition:

Messer Industrial Decarbonisation-as-a-Service™

Customer journey

Assess

Identify the customer’s energy, emissions, process and production challenge.

Design

Combine gases, applications, engineering, energy and carbon-management options.

Finance

Structure long-term offtake, service fees, partnerships and available public support.

Implement

Install, supply and operate the solution.

Optimise

Use operating data and AI-supported analysis to improve performance.

Scale

Extend the successful solution across the customer’s other plants.

Result

Messer moves from molecule supplier to embedded productivity and decarbonisation partner.

Engine 5 — Capital Allocation and Portfolio Orchestration™

Messer invested €747 million in 2025, primarily in production facilities, plant modernisation and decarbonisation-related technologies.

Every major investment should compete through a transparent regional capital-allocation model.

Investment Score

- contracted demand;

- customer credit quality;

- energy risk;

- pass-through strength;

- expected ROCE;

- free-cash-flow timing;

- network synergies;

- regulatory support;

- strategic-option value;

- downside resilience.

Capital priorities

Sustain

Protect safety, reliability and licence to operate.

Optimise

Upgrade energy efficiency and network performance.

Scale

Expand proven, contracted growth platforms.

Transform

Invest selectively in hydrogen, carbon management and digital capabilities.

Stop

Exit or redesign projects without sufficient demand, margin protection or strategic value.

Engine 6 — Regional Influence and Opportunity Intelligence™

Messer should maintain a continuous view of:

- national industrial policies;

- electricity-relief programmes;

- hydrogen funding;

- major customer investments;

- competitor projects;

- acquisition candidates;

- industrial-site closures;

- new semiconductor, battery and steel projects;

- healthcare procurement;

- geopolitical and supply-chain risk.

This is where the RapidKnowHow® Industrial Gas DACH/CEE Influence Map™ becomes operational.

It is not only a market map.

It becomes an early-warning and opportunity-conversion system.

7. Messer DACH/CEE AI-Orchestrator Command Center™

The Command Center should provide one executive view of the region.

Dashboard 1 — Energy and Margin

- electricity exposure by plant;

- current and forecast energy cost;

- pass-through recovered versus required;

- margin at risk;

- recommended pricing actions.

Dashboard 2 — Production and Network

- plant utilisation;

- energy efficiency;

- external purchases;

- logistics cost;

- cross-border optimisation opportunities;

- reliability risks.

Dashboard 3 — Customer and Commercial Value

- revenue and margin by customer;

- contract renewal pipeline;

- customer risk;

- share-of-wallet;

- decarbonisation opportunity;

- top executive actions.

Dashboard 4 — Growth and Decarbonisation

- hydrogen opportunities;

- carbon-management projects;

- new on-site plants;

- application-technology pipeline;

- public-funding potential;

- probability of conversion.

Dashboard 5 — Capital and FCF

- capital employed;

- project ROCE;

- free-cash-flow forecast;

- net-debt implications;

- project stage gates;

- stop, sustain, scale or accelerate decision.

Dashboard 6 — Competitor and Influence Radar

- Linde;

- Air Liquide;

- Air Products;

- SOL;

- SIAD;

- local competitors;

- government actions;

- customer investments;

- acquisition signals.

Dashboard 7 — Executive Action Tracker

- decision;

- owner;

- deadline;

- expected value;

- implementation status;

- realised value.

8. The 2026–2030 Transformation Roadmap

Phase 1 — Prove the Model

July–December 2026

Select a limited DACH/CEE pilot.

Recommended pilot scope:

- Germany;

- Austria;

- Poland;

- Czechia;

- Hungary;

- Serbia.

Build a minimum viable Command Center around:

- energy exposure;

- contract pass-through;

- plant-network utilisation;

- top customer profitability;

- investment pipeline;

- competitor and funding signals.

Required outputs

- common data definitions;

- top 20 value opportunities;

- top 10 margin risks;

- top five capital-allocation decisions;

- monthly executive value report.

2026 decision

Does the model generate measurable value quickly enough to justify regional scaling?

Phase 2 — Establish Regional Leadership

2027

Expand the system across the principal DACH/CEE businesses.

Introduce:

- regional Energy Control;

- Commercial Excellence;

- Network Optimisation;

- Customer Decarbonisation Pipeline;

- Capital Decision Board;

- AI-Orchestrator leadership training.

2027 target outcome

Every major regional decision is supported by:

- one source of decision truth;

- an explicit value case;

- a named owner;

- an implementation deadline;

- a realised-value measure.

Phase 3 — Scale the Customer Platform

2028

Launch integrated offers for selected sectors:

- steel and metals;

- chemicals;

- food and beverage;

- healthcare;

- electronics;

- automotive and advanced manufacturing.

Convert gas applications into repeatable sector solutions.

2028 target outcome

Messer becomes recognised not only as a gas supplier but as a:

Regional industrial productivity and decarbonisation partner.

Phase 4 — Build the DACH/CEE Ecosystem

2029

Connect Messer with:

- renewable-power suppliers;

- technology partners;

- engineering firms;

- industrial customers;

- public-funding institutions;

- universities;

- logistics partners;

- selected acquisition targets.

2029 target outcome

Messer orchestrates a network that competitors cannot easily reproduce through plant investment alone.

Phase 5 — Confirm Leadership

2030

Messer should be able to demonstrate:

- superior regional decision speed;

- strong energy and pass-through discipline;

- higher network utilisation;

- measurable customer productivity;

- bankable decarbonisation solutions;

- disciplined investment returns;

- sustained free-cash-flow growth;

- a recognised DACH/CEE AI-Orchestrator leadership position.

9. Illustrative Value-Creation Potential

The following is a RapidKnowHow strategic scenario, not Messer guidance or a financial forecast.

Based on Messer’s current scale, an integrated AI-Orchestrator programme could target an annual gross value pool of approximately:

| Value Engine | Illustrative Annual Potential |

|---|---|

| Energy procurement and operating optimisation | €30–70 million |

| Pricing and pass-through effectiveness | €25–60 million |

| Production-network and logistics optimisation | €20–45 million |

| Reliability and maintenance improvement | €15–30 million |

| Customer and product-mix improvement | €20–50 million |

| Capital-allocation discipline | €15–40 million |

| New decarbonisation contribution | €20–75 million |

| Potential annual gross value pool | €145–370 million |

These categories may overlap and should not be treated as automatically additive.

A credible executive ambition would be:

Capture €150–250 million of recurring annual value by 2030

after allowing for overlap, implementation cost and unsuccessful initiatives.

Additional cash could be released through:

- working-capital reduction;

- lower external gas purchases;

- deferred low-return capital expenditure;

- disposal or redesign of non-strategic assets.

10. The Compounding FCF Model

Year 1

Find and capture visible leakage.

- energy;

- pass-through;

- logistics;

- contracts;

- capital.

Year 2

Standardise the successful decisions.

- shared methods;

- regional data;

- executive routines;

- repeatable dashboards.

Year 3

Turn internal capability into customer value.

- productivity solutions;

- decarbonisation;

- long-term service models;

- higher switching barriers.

Year 4

Build the regional ecosystem.

- technology;

- power;

- finance;

- infrastructure;

- strategic partnerships.

Year 5

Convert superior intelligence into sustained competitive advantage.

The compounding loop becomes:

Better Signals

→ Better Decisions

→ Faster Actions

→ Higher FCF

→ More Strategic Investment

→ Stronger Customer Position

→ Better Signals

11. Why Messer Can Win

1. Private Ownership

Messer can potentially take a longer strategic view than organisations dominated by quarterly capital-market expectations.

2. Regional Heritage

Its presence and identity across Europe create customer and institutional credibility.

3. Local-for-Local Model

The existing operating philosophy supports regional resilience and customer proximity.

4. Meaningful Scale

Messer is large enough to finance technology, infrastructure and acquisitions.

5. Strategic Agility

It may be able to move faster than larger global competitors when the opportunity is specifically regional.

6. Existing Decarbonisation Assets

Hydrogen, oxy-fuel, carbon management and application technologies provide a real base—not merely a strategic presentation.

7. Leadership Transition

Messer announced a planned CEO transition and changes in European leadership in May 2026 following major changes in ownership, financing, governance and the global operating model. This creates an unusual window to embed an AI-Orchestrator system into the next leadership phase.

12. What Could Prevent Success?

Technology Without Governance

Dashboards will not create value unless executives change decisions and actions.

Fragmented Country Interests

Local optimisation may conflict with the best DACH/CEE regional decision.

Poor Data Quality

Inconsistent definitions can destroy trust in the system.

AI Without Industrial Judgement

Generic AI cannot replace gas-industry expertise.

Too Many Pilots

A large number of experiments without one accountable value programme will dissipate resources.

Hydrogen Optimism Without Contracts

No project should proceed without credible demand, risk allocation and return logic.

Failure to Measure Realised Value

Identified opportunities are not free cash flow.

Only implemented and verified results create value.

13. The Governance Model

Supervisory Board

Approves the 2030 AI-Orchestrator ambition and value guardrails.

Executive Management Board

Owns total value creation and strategic priorities.

DACH/CEE AI-Orchestrator Leader

Owns the integrated regional system.

Six Value Owners

- Energy;

- Commercial;

- Network;

- Customer Decarbonisation;

- Capital;

- Influence Intelligence.

Country Leaders

Execute within a shared regional decision framework.

Finance

Verifies realised EBITDA and free cash flow.

Human Experts

Challenge assumptions and make accountable decisions.

AI

Detects, compares, simulates and tracks.

14. First 100 Days

Decision 1

Nominate one accountable DACH/CEE AI-Orchestrator sponsor.

Decision 2

Select six pilot countries and ten priority sites.

Decision 3

Create a baseline for:

- electricity;

- pass-through;

- production cost;

- logistics;

- customer contribution;

- capital employed;

- free cash flow.

Decision 4

Identify the top 20 value opportunities.

Decision 5

Launch the six Command Center dashboards.

Decision 6

Run a weekly 60-minute AI-Orchestrator Decision Meeting.

Decision 7

Select three customer decarbonisation lighthouse cases.

Decision 8

Stop or redesign the weakest capital projects.

Decision 9

Verify realised value monthly through Finance.

Decision 10

Decide after 100 days whether to scale across DACH/CEE.

15. RapidKnowHow® Commercial Proposition

The Offer

Messer DACH/CEE AI-Orchestrator Opportunity Sprint™

Four-Week Executive Decision Engagement

Week 1 — Discover

- current operating model;

- strategic assets;

- value leakage;

- regional opportunities;

- leadership priorities.

Week 2 — Assess

- energy exposure;

- commercial effectiveness;

- network economics;

- capital pipeline;

- influence environment.

Week 3 — Design

- Command Center;

- six value engines;

- governance;

- scorecards;

- implementation priorities.

Week 4 — Decide

- top five executive decisions;

- 100-day action plan;

- 2026–2030 roadmap;

- value case;

- scale decision.

Deliverables

- DACH/CEE Influence Map;

- AI-Orchestrator Maturity Assessment;

- Value-Creation Map;

- Executive Decision Dashboard;

- 100-Day Action Guide;

- 2030 Strategic Roadmap.

Final Strategic Verdict

Messer has already built a strong, resilient and profitable international industrial-gas company.

The next value-creation step is not simply to add more plants.

It is to connect the existing plants, energy, contracts, customers, applications, people and capital through one superior regional decision system.

The 2030 Winning Position

Messer becomes the privately controlled industrial-gas company that makes faster, more locally grounded and more economically disciplined decisions than any competitor in DACH/CEE.

That is the essence of AI-Orchestrator leadership.

RapidKnowHow® Power Sentence

Linde leads through global scale.

Air Liquide leads through European system strength.

Messer can lead DACH/CEE through regional intelligence, customer proximity, decision speed and disciplined capital orchestration.

Signal → Intelligence → Decision → Action → FCF → Compounded Leadership

RapidKnowHow® – Making Industrial Gas Value Creation Visible™

Important Qualification

This report is an independent RapidKnowHow strategic analysis based on publicly available information. It is not commissioned, endorsed or approved by Messer SE & Co. KGaA and does not contain confidential Messer information. Financial value ranges are illustrative strategic scenarios, not Messer forecasts.