Industrial Gas Organisation Design (1925–2035)

What Worked • Who Led • What Wins Next

A) 100 Years Evolution of Competitive Organisation Design

1. 1920s–1950s: Engineering-Centric Industrial Model

Design

- Centralized, plant-driven

- Engineering + production dominance

- Local/regional supply

Leaders

- Linde plc

- Air Liquide

- AGA AB

Why it worked

- Scarcity of industrial gases

- High technical barriers

- Demand from steel, chemicals, welding

👉 Winning Formula:

Engineering Excellence + Asset Control

2. 1960s–1980s: Scale & Vertical Integration Model

Design

- Large-scale production plants (ASUs)

- Long-term contracts (on-site supply)

- Vertical integration (production → delivery)

Leaders

- Air Products and Chemicals

- Praxair

Why it worked

- Economies of scale

- Lock-in contracts (10–20 years)

- Capital intensity = barrier to entry

👉 Winning Formula:

Scale + Long-Term Contracts + Capital Power

3. 1990s–2010: Global Efficiency & Consolidation Model

Design

- Global matrix organizations

- Regional hubs + shared services

- M&A-driven consolidation

Leaders

- Linde plc

- Air Liquide

- Praxair

Why it worked

- Cost optimization

- Global customer contracts

- Standardization across regions

👉 Winning Formula:

Global Scale + Cost Leadership + Integration

4. 2010–2025: Portfolio & Financial Performance Model

Design

- Portfolio-based business units (On-site, Bulk, Packaged, Healthcare)

- Strong KPI governance (ROCE, FCF)

- Selective growth (Hydrogen, Healthcare)

Leaders

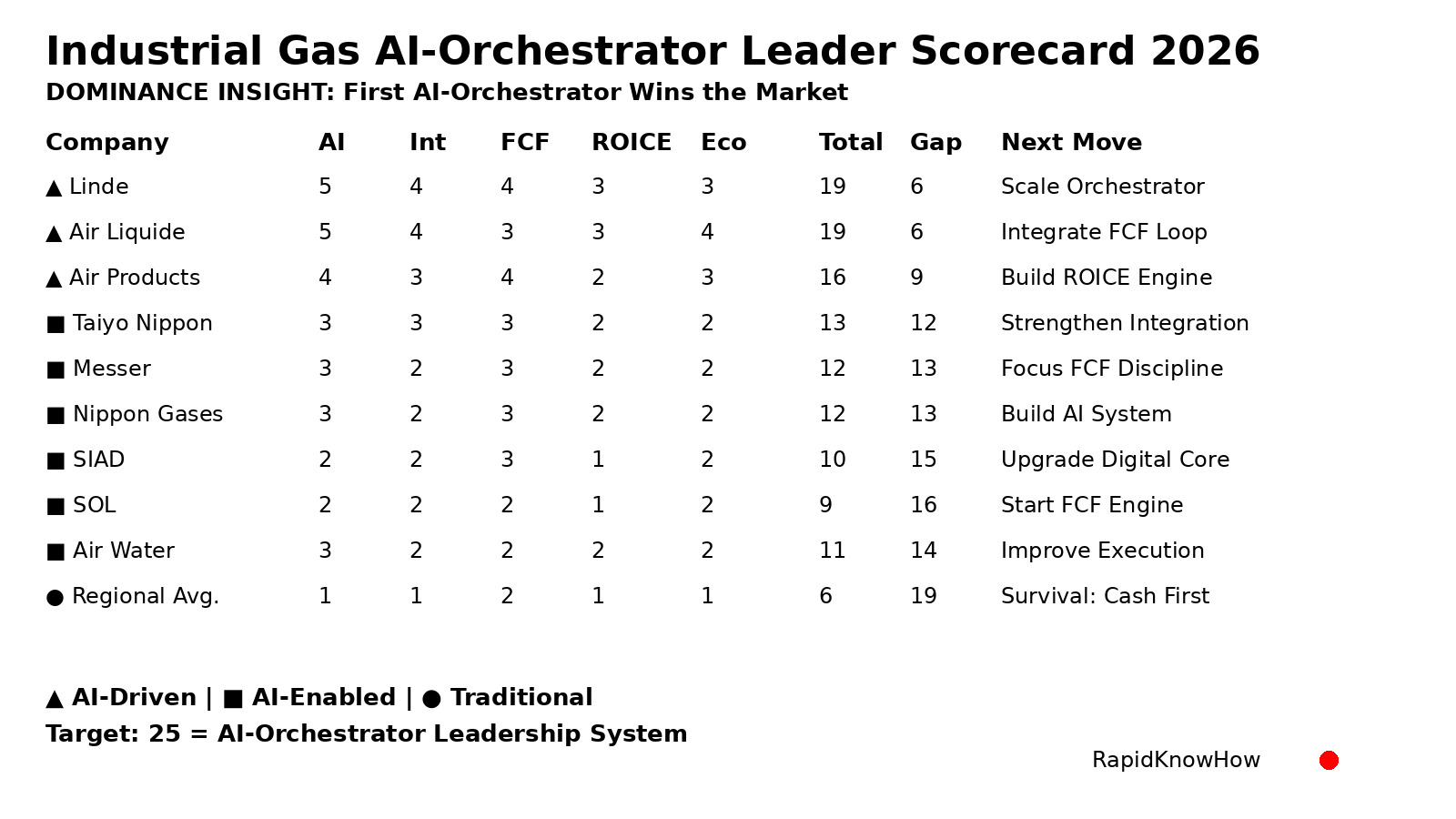

- Linde plc (clear #1)

- Air Liquide

Why it worked

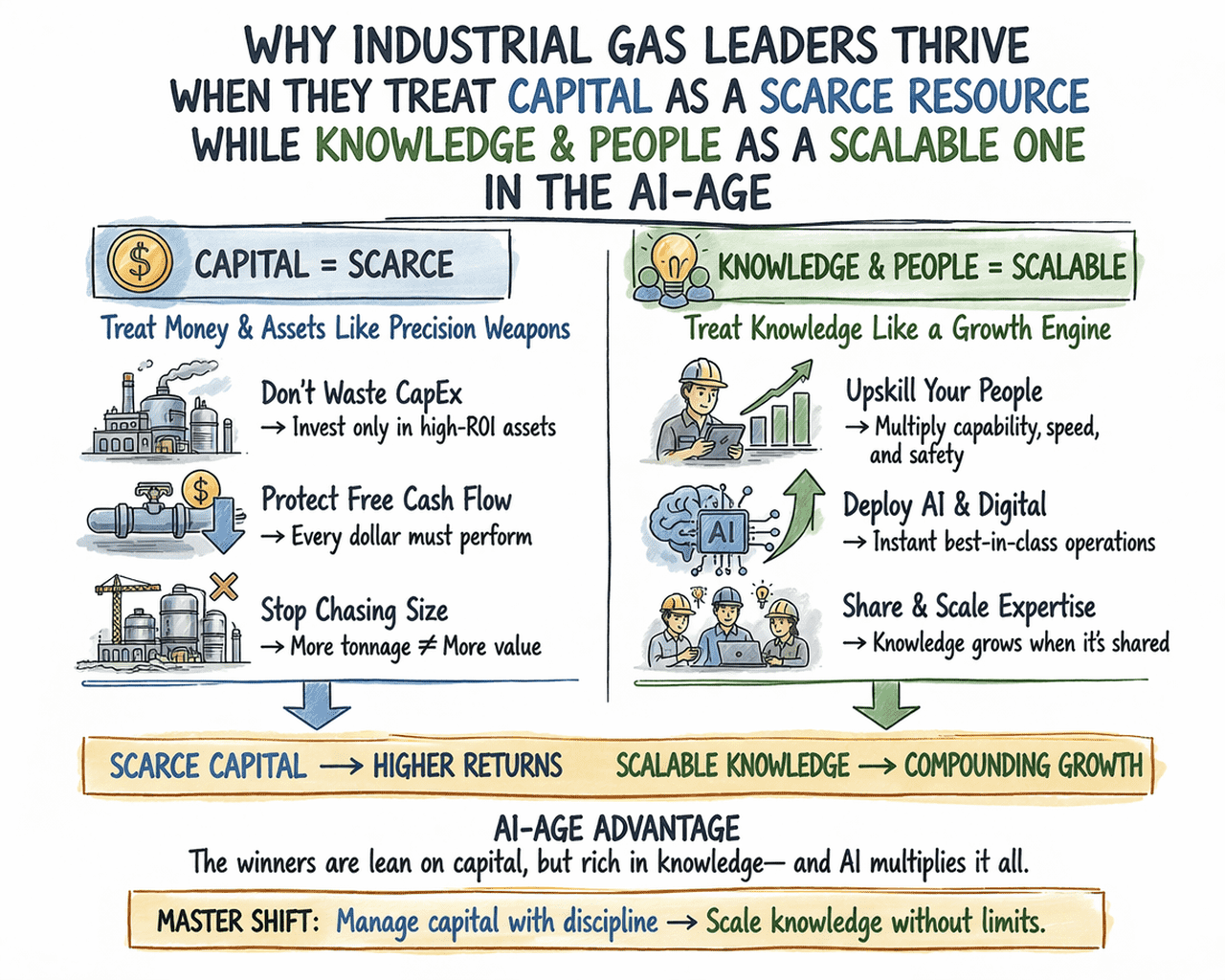

- Capital discipline

- High-margin portfolio steering

- Focus on resilient cash flows

👉 Winning Formula:

FCF + ROCE + Portfolio Optimization

B) The Emerging Winning Model (2025–2035)

AI-Orchestrator + Asset-Light Ecosystem Model

Design

- AI-Orchestrator at the center (decision intelligence)

- Asset-light partner ecosystems

- Platform-based service model (Gas-as-a-Service)

Core Shift

From:

- Owning assets

To: - Orchestrating value flows

Why this model will dominate

1. Speed beats scale

- Traditional: 3–5 years investment cycle

- New: weeks/months deployment

2. Data > Assets

- AI optimizes:

- Pricing

- Logistics

- Demand prediction

3. Customers want outcomes, not gas

- Oxygen uptime

- Hydrogen decarbonization

- Healthcare continuity

👉 Winning Formula (Next 10 Years)

AI × Ecosystem × FCF Velocity

C) Who Will Thrive — and HOW

1. The Winners (2025–2035)

1.1 Incumbents who transform

- Linde plc

- Air Liquide

IF they:

- Build AI-Orchestrator systems

- Shift to platform + services

- Open ecosystems

1.2 New Asset-Light Challengers

- Regional players

- Digital-first operators

- Hydrogen ecosystem builders

Advantage

- No legacy assets

- Faster decision cycles

1.3 Tech-driven Integrators

- AI + energy + gas convergence players

- Industrial platform companies

2. Who Will Lose

❌ Asset-heavy, slow decision organizations

❌ Pure product sellers (gas volume mindset)

❌ Organizations without digital intelligence

3. HOW to Thrive (CEO Playbook)

Step 1 — Shift the Core Logic

From:

- Product → Volume

To: - Outcome → Value

Step 2 — Build AI-Orchestrator Core

- Real-time decision engine:

- Pricing

- Supply chain

- Asset utilization

Step 3 — Go Asset-Light

- Partner instead of owning everything

- Build ecosystems:

- Logistics

- Energy

- Healthcare

Step 4 — Monetize FCF Velocity

- Faster cash cycles

- Dynamic pricing

- High-margin services

Step 5 — Create Platform Dominance

- Gas-as-a-Service

- Subscription models

- Integrated solutions

🔥 FINAL STRATEGIC SNAPSHOT (CEO LEVEL)

1925–1980

➡️ Win by Engineering + Scale

1980–2025

➡️ Win by Global Efficiency + FCF Discipline

2025–2035

➡️ Win by:

👉 AI-Orchestrator Leadership + Ecosystem Control + Speed

Strategic Sentence

👉 “The winner is no longer the one who owns the most gas plants — but the one who makes the smartest decisions fastest.” – Josef David