Germany’s competitiveness problem is not one dramatic collapse. It is a long slowdown.

The visible symptoms are familiar: weak growth, fragile industrial momentum, slower productivity gains, skills shortages, and pressure from higher energy and regulatory costs.

The deeper issue is that Germany’s historic strengths — engineering depth, industrial discipline, and process quality — are no longer sufficient when speed, digital scaling, AI adoption, and rapid capital renewal matter more than before. Germany has not simply become weak. It has become too slow relative to the pace of structural change.

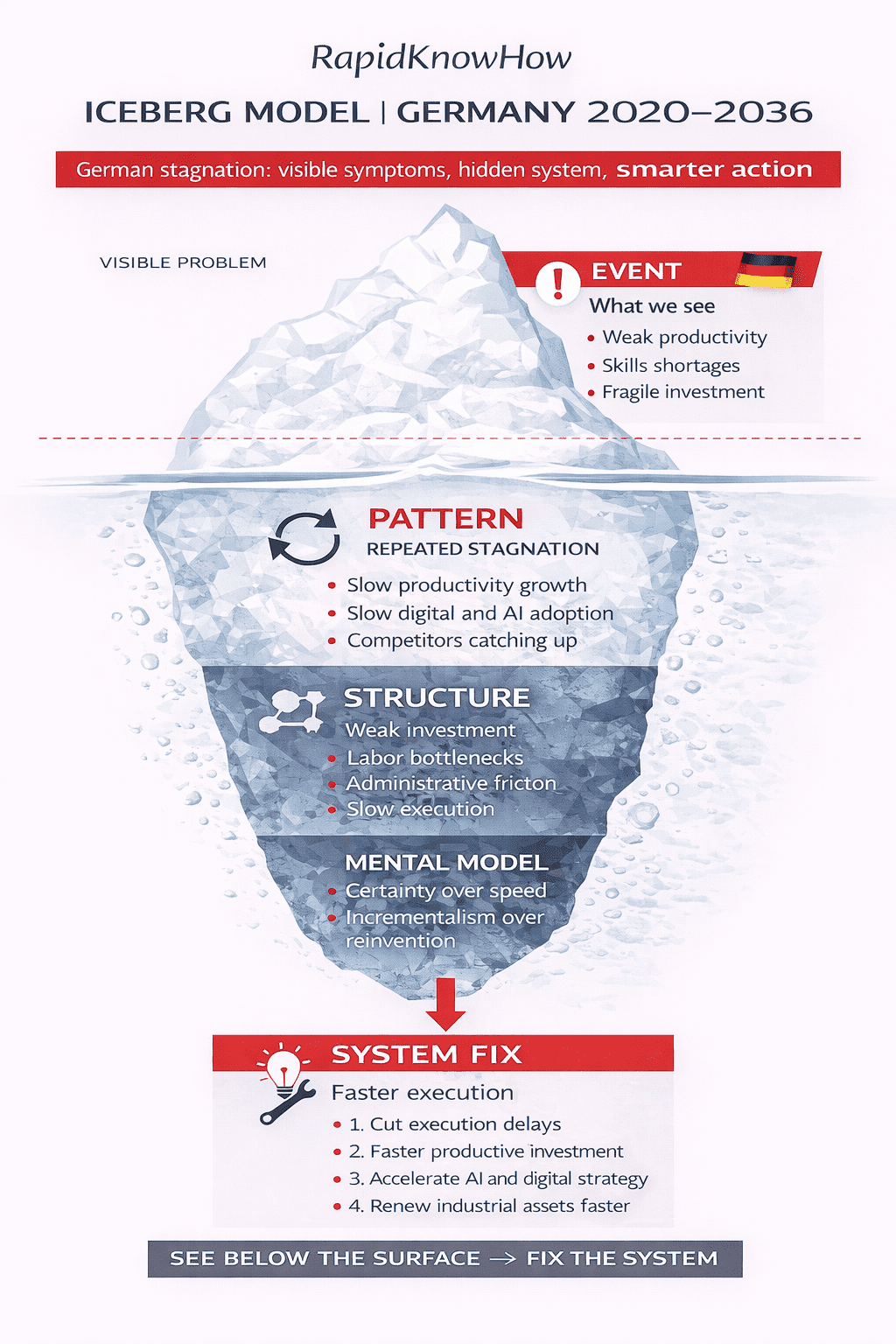

Event — what we see.

From 2020 through 2025, Germany experienced repeated stagnation rather than a strong rebound. The OECD notes that growth had already slowed before the pandemic and energy crisis, and that the slowdown in potential growth has been driven by weak investment, a shrinking working-age population, and declining productivity growth. The Bundesbank also described 2025 as another year of near-stagnation, which would mean three consecutive years of minimal growth. In plain language: the visible problem is not only lower output. It is lower momentum.

Pattern — what keeps repeating.

The pattern is repeated stagnation.

Germany absorbs a shock, stabilizes, but does not regain strong forward movement.

Productivity underperforms, digital and AI adoption remain uneven, labor shortages keep acting as a bottleneck, and investment appetite stays restrained.

KfW also points to persistent pressure on Germany’s international competitiveness as a business location, while the OECD highlights that skilled labor shortages are becoming a major bottleneck for both growth and the green and digital transitions.

Structure — what drives the pattern.

The structural layer has four parts.

First, Germany faces weak investment and declining productivity growth.

Second, demographic pressure is shrinking the working-age population and tightening skilled labor availability.

Third, the system remains burdened by administrative friction, regulatory complexity, and slow execution.

Fourth, many firms — especially in the Mittelstand — still innovate, but not at the pace required to turn capability into broad national acceleration.

KfW’s 2025 SME Innovation Report is encouraging in that the share of innovators rose to 41% in 2022–2024, but “marginally lower” than 2018–2020 is still not a breakout innovation wave.

The structure is therefore not broken in a dramatic sense. It is too heavy, too fragmented, and too slow to compound advantage.

Mental model — what sustains the structure.

Germany’s hidden mental model can be summarized like this:

quality first, order first, certainty first.

That logic was a strength for decades. But today it can turn into a brake.

When a system believes that incremental optimization is safer than rapid reinvention, that compliance is safer than experimentation, and that industrial excellence alone will protect competitiveness, the result is not disaster overnight.

The result is gradual relative decline. This is consistent with the OECD’s diagnosis that

Germany needs to revive business dynamism and productivity growth, not merely preserve existing strengths.

System fix — what changes the outcome.

Germany does not need cosmetic repair.

It needs an upgrade from an efficiency-led model to an adaptability-led model.

That means faster permitting and execution, stronger labor-force participation and skills policy, faster AI and digital adoption, deeper incentives for productive investment, and a more aggressive push to renew industrial assets and business models.

The OECD explicitly points to stronger competition, higher business dynamism, better labor-supply incentives, and action on skilled labor shortages.

The European Commission’s AI strategy materials and wider EU work on AI adoption also support the point that faster diffusion of AI is now central to competitiveness.

2026–2036 outlook.

If Germany keeps the current model, the likely decade ahead is one of managed erosion: respectable institutions, world-class niches, but weaker aggregate momentum and more difficulty defending industrial leadership.

If Germany upgrades the system, the next decade can look different: not a return to the old export machine, but a newer model built on AI-enhanced industry, energy resilience, faster capital renewal, workforce upskilling, and simpler execution.

The critical question is not whether Germany still has capability. It does.

The real question is whether it can convert capability into speed.

RapidKnowHow One-line conclusion.

Germany’s competitiveness challenge is an iceberg problem: visible stagnation above the surface, slow structure and cautious mental models below it.

Change the system, and the visible results can change again.

ICEBERG MODEL | GERMANY 2026–2036

German stagnation: visible symptoms, hidden system, smarter action

15-Second Insight

Germany is not out of capability. It is losing speed.

Core Diagnosis

The problem is not one shock. The problem is a repeated stagnation pattern driven by slow adaptation, labor bottlenecks, weak productivity growth, and heavy execution friction.

Do not fix the event only. Redesign the system that keeps reproducing the event.

Weak industrial momentum, slow productivity growth, fragile investment, skills shortages, and pressure on competitiveness.

Repeated stagnation: recovery remains weak, digital and AI adoption stay uneven, and global competitors gain relative ground.

Weak investment, declining productivity growth, shrinking working-age population, skilled labor shortages, and administrative friction.

Quality first. Certainty first. Incremental improvement over rapid reinvention.

Upgrade from efficiency-led strength to adaptability-led strength: faster permitting, stronger skills policy, AI adoption, productive investment, and quicker industrial renewal.

1) Cut execution delays. 2) Raise productive investment. 3) Accelerate AI and digital adoption. 4) Expand skilled labor supply and reskilling. 5) Renew industrial assets faster.

Germany’s challenge is not lack of strength; it is lack of speed in converting strength into future competitiveness.

Leave a Reply