One Urgent Problem. One Clear Decision. One Measurable Result.

See Earlier • Decide Better • Act Faster

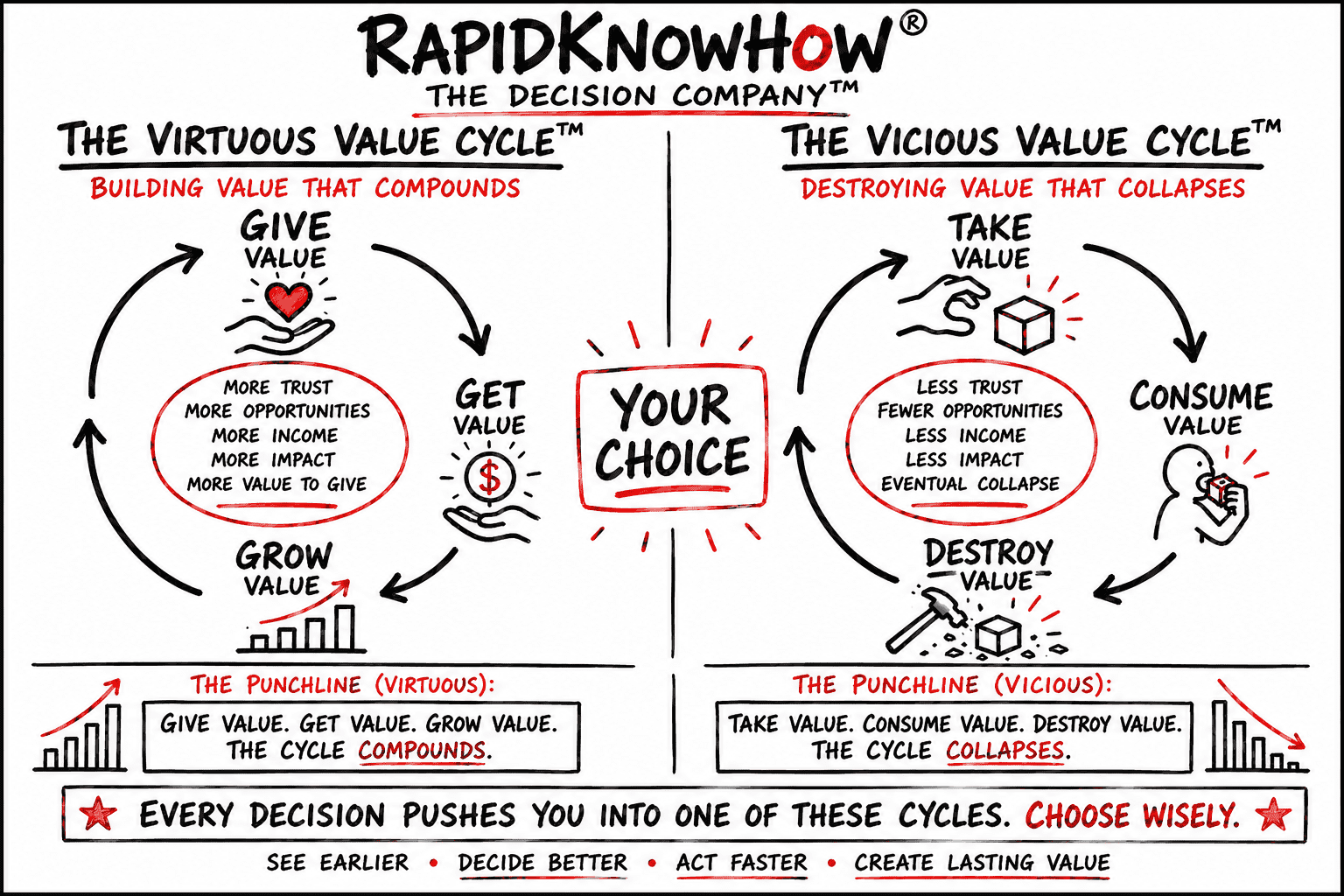

RapidKnowHow® — THE DECISION COMPANY™

RapidKnowHow® — THE DECISION COMPANY™

ONE URGENT PROBLEM. ONE CLEAR DECISION. ONE MEASURABLE RESULT.

See Earlier • Decide Better • Act Faster

RapidKnowHow® helps leaders and professional advisors turn complex situations into clear decisions, executable actions and measurable value.

Choose Your Path

Two ways to create measurable value.

Path A

I LEAD A COMPANY

Solve ONE urgent strategic problem.

When cash flow, growth, competitiveness, investment or execution is at stake, complexity slows decisions.

ONE SIGNAL → ONE INSIGHT → ONE DECISION → TOP 3 ACTIONS → ONE RESULT

Start with the decision. Prove the value. Integrate what works.

Explore the Corporate Decision Path →Path B

I ADVISE COMPANIES

Turn ONE successful assignment into recurring client value.

Many independent consultants win a project, deliver good work, invoice — and leave.

ONE JOB → ONE RESULT → ONE PROCESS → ONE RHYTHM → RECURRING VALUE

Integrate the value-creation process — not personal dependency.

Explore the License Partner Path →The RapidKnowHow® Decision System

Complexity becomes executable.

What materially changed?

Why does it matter?

What must be decided now?

What happens next?

What measurable outcome demonstrates progress?

Define, measure and verify the value created.

Corporate Key Account Path

From urgent problem to institutional capability.

URGENT PROBLEM → ONE DECISION EXPERIENCE™ → BUSINESS CASE → PROVE VALUE → INTEGRATE → INSTITUTIONAL LICENSE → COMPOUND VALUE

The objective is a transferable decision system that continues creating value inside the organisation.

Consultant License Partner Path

From project work to recurring value partnership.

The consultant should not become indispensable. The value-creation system should.

Strategic Key Account Management MASTER™

Inbound + Outbound. ONE value partnership engine.

Inbound KAM

They discover RapidKnowHow®.

ATTRACT → SELF-SELECT → QUALIFY → EXPERIENCE

↓

INTEGRATE

↓

LICENSE

↓

COMPOUND

Outbound KAM

RapidKnowHow® selects them.

SELECT → SIGNAL → ENGAGE → EXPERIENCE

The Value Partnership Principle

Create value before asking for value.

RapidKnowHow® does not begin with a product pitch. It begins with a strategically relevant problem.

GIVE VALUE → GET FAIR VALUE → GROW VALUE → COMPOUND VALUE

Confidential Mandate Check

Is there a strategic fit?

A potential mandate should answer five questions.

If the situation is strategically relevant, measurable and actionable, that is the right place to begin.

Start a Confidential Conversation →