Week 20, 2026

Business • Geopolitics • Life

RapidKnowHow GeoPulse™ Rolling Forecast System

Executive Summary

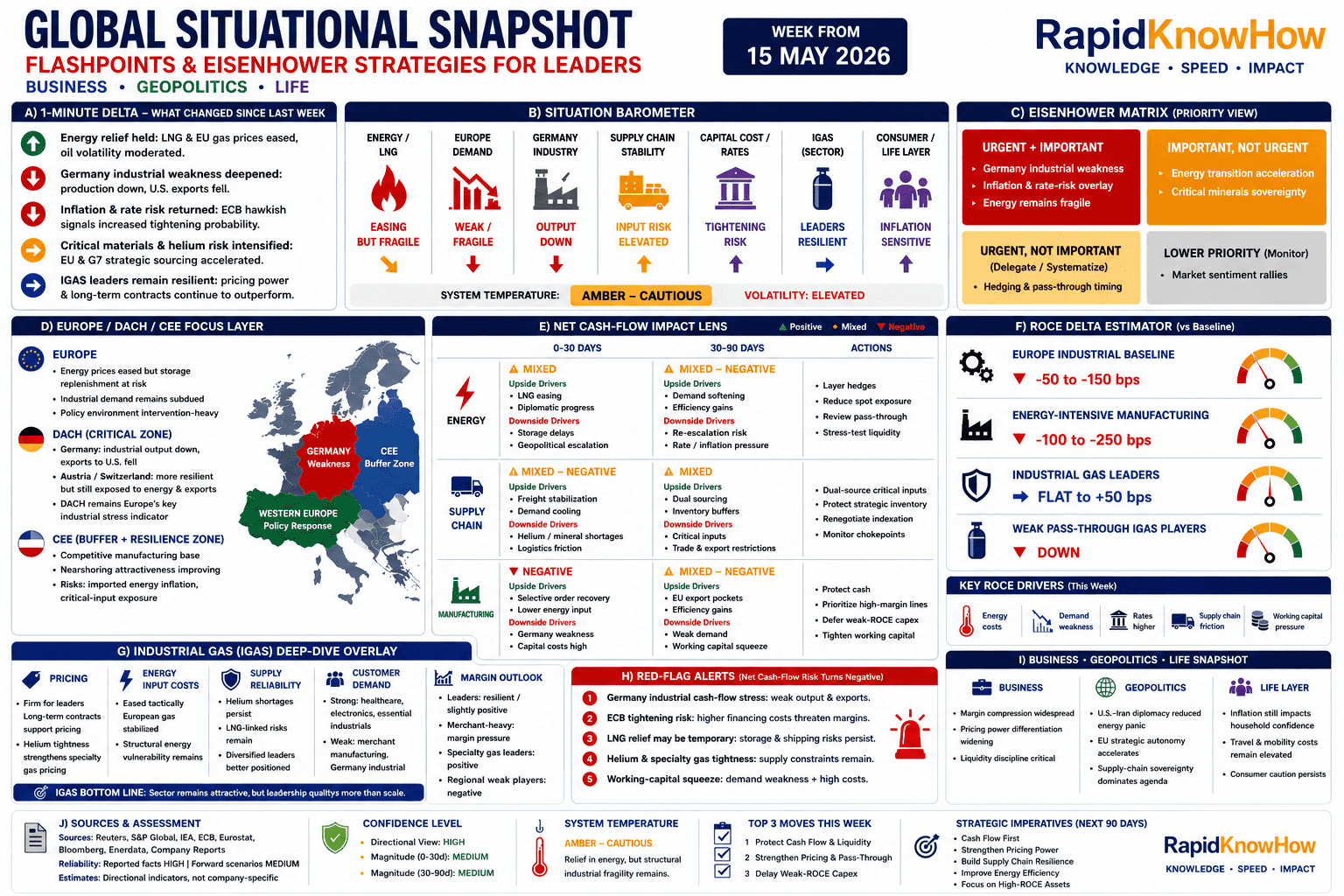

Week 20, 2026 marks a transition from acute energy panic toward a more dangerous and persistent phase: embedded industrial fragility under elevated capital and energy costs.

While tactical relief appeared in LNG and gas markets, the structural pressure on European industry intensified. Germany’s industrial production weakened again, exports to the U.S. fell sharply, and ECB rhetoric shifted more hawkish due to inflation persistence. The implication is clear:

The primary management challenge is no longer surviving a shock event.

It is preserving cash flow, protecting ROCE, and maintaining pricing power during prolonged structural volatility.

The operating environment remains defined by five interacting forces:

- Elevated but unstable energy costs

- Weakening industrial demand in Europe

- Tightening financing conditions

- Fragile strategic supply chains

- Growing separation between strong and weak business models

Industrial Gas (IGAS) leaders continue to outperform due to:

- disciplined pricing,

- long-term contracts,

- helium/specialty positioning,

- diversified supply structures,

- and stronger pass-through governance.

However, weaker merchant-heavy or energy-exposed operators are increasingly vulnerable to margin erosion and working-capital stress.

1. Global Situation Overview

Energy Markets

The most positive development this week was the easing of LNG and European gas prices. Markets reacted to renewed hopes of a U.S.–Iran diplomatic breakthrough and lower Northeast Asian LNG demand.

However, the relief remains tactical rather than structural.

Europe still faces:

- storage replenishment risk,

- geopolitical shipping vulnerability,

- and long-term energy-security uncertainty.

Management implication:

Companies should not interpret lower spot prices as normalization.

Energy remains a strategic volatility variable.

Europe and Germany

Germany remains the critical stress node for Europe.

Key signals:

- industrial production declined again,

- exports to the U.S. weakened materially,

- imports surged,

- the trade surplus compressed.

This matters because Germany acts as:

- Europe’s industrial confidence anchor,

- demand engine,

- and supply-chain stabilizer.

When Germany weakens, the entire European manufacturing ecosystem feels the pressure.

For Boards and leadership teams, this means:

- slower industrial order cycles,

- weaker fixed-cost absorption,

- and rising working-capital stress risk.

Inflation and Capital Costs

The ECB’s messaging became more hawkish this week.

Policymakers increasingly acknowledge that:

- energy inflation may persist longer,

- second-round inflation effects are building,

- and further tightening may become necessary.

This creates a dangerous combination:

- elevated operating costs,

- plus elevated financing costs.

The result:

- weaker investment appetite,

- tighter liquidity discipline,

- delayed capex,

- and stronger focus on ROCE quality.

2. Eisenhower Strategic Priorities for Leaders

Urgent + Important

A. Protect Cash Flow

Cash flow is now more important than growth.

Leadership focus should include:

- pricing discipline,

- working-capital optimization,

- inventory reduction,

- energy-cost governance,

- and customer-credit monitoring.

B. Strengthen Pass-Through Governance

The strongest companies in volatile periods are not necessarily the largest.

They are the companies with:

- fastest repricing capability,

- strongest contracts,

- and most disciplined commercial governance.

Pass-through effectiveness is now a strategic capability.

C. Prepare for Extended Volatility

Many organizations still operate with “temporary crisis” assumptions.

The current evidence suggests:

- volatility may persist through 2026,

- energy instability remains unresolved,

- and geopolitical fragmentation is increasing.

Organizations should shift from:

- reactive crisis management

to - permanent volatility governance.

Important, Not Urgent

D. Accelerate Energy Resilience

This includes:

- electrification,

- energy efficiency,

- diversified sourcing,

- and strategic energy partnerships.

The objective is not sustainability branding alone.

The objective is:

lower structural volatility exposure.

E. Secure Strategic Inputs

Critical minerals, helium, specialty gases, semiconductors, and logistics corridors are becoming strategic assets.

Supply-chain resilience is no longer a procurement issue alone.

It is a:

- geopolitical,

- financial,

- and competitive issue.

3. Europe / DACH / CEE Assessment

Europe

Europe remains highly exposed to:

- imported energy inflation,

- industrial slowdown,

- and policy fragmentation.

At the same time, Europe is accelerating:

- industrial policy,

- strategic autonomy,

- and supply-chain resilience.

The tension between:

- high-cost industrial reality

and - long-term strategic transformation

will define the next 12–24 months.

DACH Region

Germany

Germany remains the weakest major industrial signal in Europe.

Risks:

- export softness,

- weak manufacturing output,

- elevated energy costs,

- financing pressure.

Austria

Austria remains highly energy-sensitive and export-dependent.

Industrial sectors with:

- strong contracts,

- energy pass-through,

- and specialized positioning

will remain more resilient.

Switzerland

Switzerland remains comparatively resilient due to:

- stronger financial positioning,

- high-value exports,

- and lower direct industrial exposure.

However, second-order effects remain significant.

CEE Region

CEE continues strengthening its role as:

- a manufacturing resilience zone,

- nearshoring destination,

- and cost buffer.

But the region still faces:

- imported inflation,

- energy exposure,

- and dependence on broader European demand.

4. Industrial Gas (IGAS) Strategic Assessment

Sector Position

Industrial gases remain one of the more resilient industrial sectors globally.

Why:

- essential-product positioning,

- contract structures,

- pricing power,

- diversified end markets.

Strategic Separation Is Increasing

The gap between strong and weak operators is widening.

Strong IGAS Leaders

Characteristics:

- strong pricing governance,

- long-term contracts,

- diversified supply,

- specialty gas exposure,

- disciplined capital allocation.

These companies continue protecting margins relatively well.

Weak Operators

Characteristics:

- merchant-heavy exposure,

- weak pricing power,

- poor pass-through governance,

- regional concentration,

- high energy exposure.

These firms face increasing:

- margin compression,

- working-capital pressure,

- and ROCE deterioration.

Helium and Specialty Gas Risk

Helium remains strategically fragile.

The sector continues facing:

- LNG-linked supply disruptions,

- constrained global availability,

- elevated prices.

This creates both:

- opportunity for leaders,

- and risk for exposed customers.

5. ROCE and Cash-Flow Outlook

Europe Industrial Baseline

Expected ROCE pressure:

- approximately -50 to -150 basis points.

Main drivers:

- weak demand,

- energy cost pressure,

- financing costs.

Energy-Intensive Manufacturing

Expected ROCE pressure:

- approximately -100 to -250 basis points.

Main drivers:

- power/gas costs,

- pass-through lag,

- weak utilization.

Industrial Gases

Sector outlook:

- resilient overall,

- but increasingly bifurcated.

Strong operators:

- stable to slightly positive ROCE.

Weak operators:

- deteriorating returns.

6. Strategic Actions for Boards and Leaders

Immediate (0–30 Days)

1. Protect Liquidity

- tighten working capital,

- reduce weak-margin production,

- stress-test energy exposure.

2. Lock Tactical Energy Relief

- hedge selectively,

- reduce spot dependency,

- renegotiate energy-linked clauses.

3. Prioritize High-ROCE Business

- sequence output by contribution margin,

- defer low-return capex,

- protect strategic customers.

Medium-Term (30–90 Days)

4. Strengthen Resilience Infrastructure

- dual-source critical inputs,

- secure logistics corridors,

- improve supply visibility.

5. Build Volatility Governance Systems

Install:

- rolling scenario analysis,

- early-warning indicators,

- cash-flow stress monitoring,

- ROCE governance frameworks.

6. Accelerate Energy Efficiency

Energy efficiency is no longer only sustainability policy.

It is:

a direct cash-flow and competitiveness strategy.

Final Strategic Assessment

Week 20, 2026 can be summarized in one sentence:

Tactical energy relief does not remove structural industrial fragility.

The environment remains:

- inflation-sensitive,

- geopolitically unstable,

- and operationally volatile.

The winning organizations through 2026–2030 will likely be those that:

- protect cash flow,

- govern volatility,

- maintain pricing power,

- strengthen resilience,

- and allocate capital with extreme discipline.

For Industrial Gas leaders specifically, the strategic differentiators are now clear:

- pass-through governance,

- specialty gas positioning,

- energy management,

- supply resilience,

- and disciplined ROCE protection.

RapidKnowHow GeoPulse™ Bottom Line

Volatility is no longer a temporary disruption.

It is becoming the permanent operating environment.

The objective for leadership is therefore not prediction.

The objective is:

resilient, disciplined, high-quality decision execution under uncertainty.

Sources + Assessment

Addendum to the Board & Leadership Report — Week 20, 2026

A) Main source base

1. Energy / commodity regime

The strongest source is the World Bank Commodity Markets Outlook, reported directly by the World Bank and Reuters. The key fact base is that energy prices are projected to rise 24% in 2026, with further upside risk if Middle East disruptions persist.

2. Germany / DACH industrial stress

Reuters reporting on German exporters and industrial conditions is the main source for the DACH risk layer. A DIHK survey cited by Reuters says 46% of German firms abroad see high energy prices as a key risk, and 40% cite supply-chain disruptions.

3. IGAS sector resilience

For Industrial Gases, the strongest sources are Reuters on Linde and Air Products, plus Linde’s own Q1 2026 earnings release. Linde raised the lower end of its 2026 guidance after a Q1 beat, while Air Products lifted its 2026 forecast amid stronger helium pricing.

4. CEE energy layer

Reuters reporting on CEZ shows how Middle East-driven energy prices are lifting utility profit outlooks in CEE. This supports the assessment that CEE is both exposed to imported energy volatility and strategically important as a regional energy buffer.

B) Reliability assessment

| Source cluster | Reliability | Use in report | Limitation |

|---|---|---|---|

| World Bank / Reuters energy outlook | High | Energy regime, inflation pressure, cash-flow risk | Scenario-dependent if Middle East disruption changes |

| Reuters Germany / DIHK reporting | High | DACH industrial stress, exports, supply-chain risk | Survey-based, not company-by-company proof |

| Company earnings: Linde / Air Products | High | IGAS pricing and resilience signals | Large-player view, not representative of weak regional operators |

| Linde official earnings release | Very high | Pricing, volume, productivity, operating profit facts | Company disclosure, naturally selective |

| CEZ / CEE energy reporting | Medium-high | CEE energy sensitivity and utility upside | Utility-specific, not full CEE manufacturing picture |

| ROCE / cash-flow estimates | Medium | Directional board interpretation | Model-based inference, not audited forecast |

C) What is strongly supported

The report is strongly supported on these points:

- Energy prices remain a major 2026 operating-cost risk.

- German industrial and export exposure remains under pressure from energy and supply-chain disruption.

- Large IGAS leaders are comparatively resilient due to pricing, productivity, guidance strength, and helium pricing support.

- CEE energy companies can benefit from higher electricity prices, but that does not remove industrial cost pressure.

D) What is directional assessment, not hard fact

The following elements are RapidKnowHow interpretation layers:

- ROCE delta ranges such as -50 to -150 bps or -100 to -250 bps

- Net cash-flow impact classification by 0–30 and 30–90 days

- IGAS split between “leaders” and “weak pass-through players”

- Europe / DACH / CEE strategic positioning as “fragile,” “buffer,” or “resilience zone”

These are useful for decision navigation, but they should be read as directional governance estimates, not forecasts.

E) Overall confidence level

Directional confidence: High

Magnitude confidence: Medium

Company-specific applicability: Requires case-by-case validation

Best use: Board discussion, scenario planning, cash-flow stress testing, ROCE governance review

Final reliability statement

The Week 20 Report is solid for strategic decision framing. The strongest factual basis is energy-price risk, German/DACH exposure, and IGAS leader resilience. The ROCE and cash-flow estimates should be treated as structured board-level indicators, not precise financial forecasts.