CEE Focus 2026 — Power Report

1. Executive Core

Central and Eastern Europe is entering a decisive industrial phase in 2026. The region sits between Western European demand, Ukrainian war pressure, German industrial weakness, energy volatility, EU reindustrialisation policy, and the need for strategic autonomy.

For industrial gas companies, CEE is no longer simply a regional sales territory. It is becoming a strategic flow zone.

The key question is:

Who secures oxygen, nitrogen, hydrogen, argon, CO₂, helium and specialty gas flows for CEE industry — and who turns these flows into customer resilience, decarbonisation and free cash flow?

Industrial gases are invisible but essential. Without them, steel plants, food processors, hospitals, semiconductor fabs, chemical plants, refineries, welding operations, water-treatment systems and hydrogen projects cannot operate safely, efficiently or competitively.

CEE 2026 creates one clear strategic opportunity:

Move from gas supplier to Industrial Gas AI-Orchestrator for resilient industry.

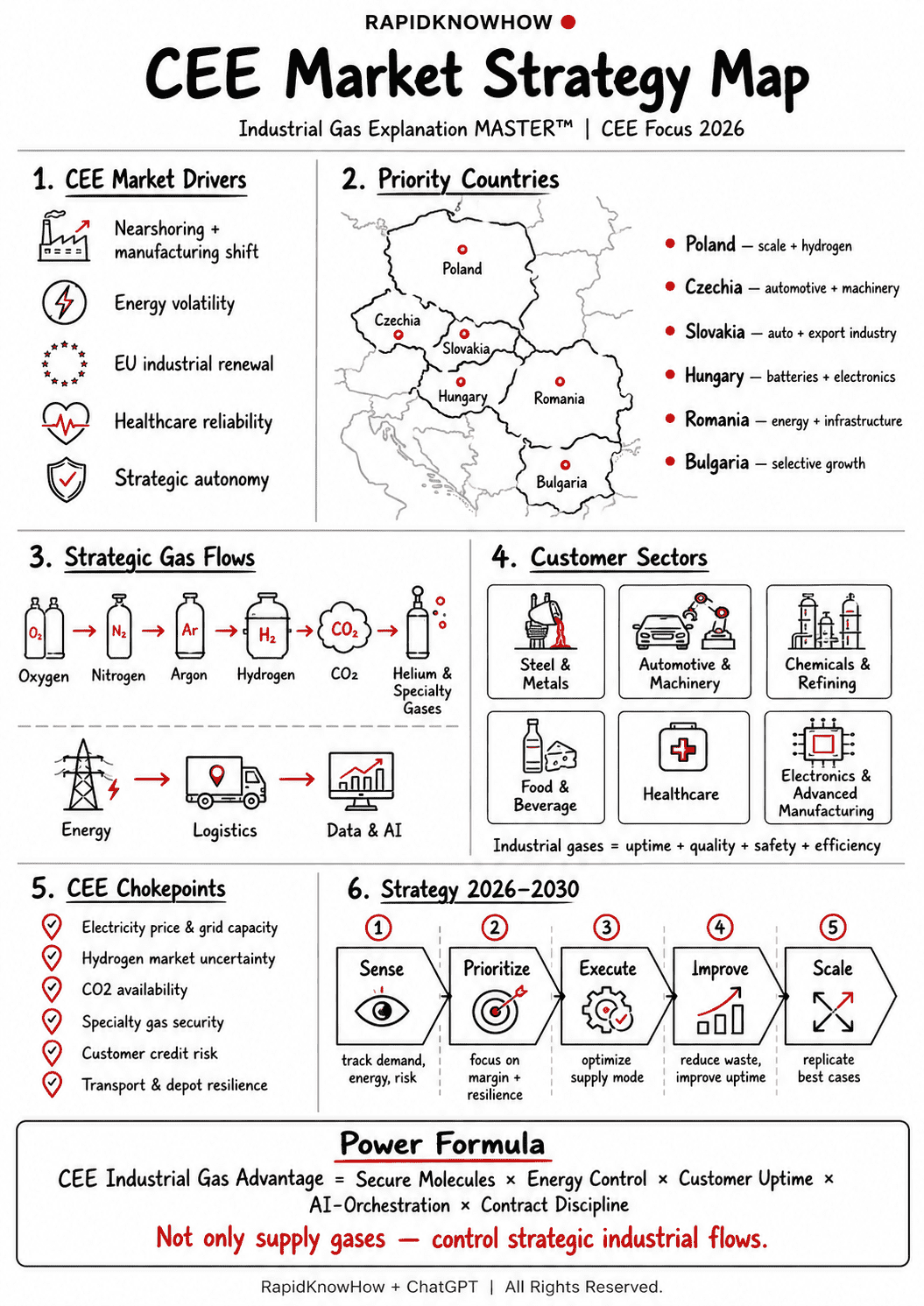

2. Why CEE Matters in 2026

CEE matters because it combines five industrial advantages:

- Manufacturing depth

CEE remains tightly connected to automotive, machinery, electronics, metals, chemicals, construction materials and export manufacturing. - Nearshoring potential

Western European companies want shorter, safer and more controllable supply chains. CEE offers geographic proximity, industrial skills and lower structural cost than many Western markets. - EU funding and infrastructure renewal

EU structural and recovery funds continue to support investment in infrastructure, energy systems, innovation and industrial modernisation. OECD’s 2026 outlook for Czechia, for example, expects investment to remain robust in 2026 due to EU structural and recovery funds, even while energy prices and uncertainty weigh on consumption and confidence. - Energy-security pressure

CEE remains highly exposed to energy-price volatility, supply-chain disruption and geopolitical risk. The European Commission’s Spring 2026 forecast explicitly frames the EU outlook around slower growth as a new energy shock drives inflation and damages confidence. - Strategic-autonomy relevance

CEE is close to Ukraine, the Black Sea, Central European manufacturing corridors and EU defence-industrial renewal. That makes industrial resilience in the region a geopolitical and economic priority.

3. The Industrial Gas Demand Engine

CEE industrial gas demand is driven by six customer clusters.

Cluster 1 — Metals and steel

Oxygen is used in steelmaking, cutting, combustion enrichment and process efficiency. Nitrogen and argon support inerting, heat treatment and metallurgical quality. As Europe seeks cleaner steel, hydrogen and oxygen become increasingly important.

Cluster 2 — Automotive and machinery

CEE’s automotive and supplier base needs welding gases, laser cutting gases, heat-treatment atmospheres, nitrogen, argon and specialty applications. Electric and hybrid vehicle growth strengthens demand for precision manufacturing gases.

Cluster 3 — Chemicals, refining and energy

Hydrogen, oxygen, nitrogen and CO₂ are central to refineries, petrochemicals, chemical processing, sulfur removal, inerting and decarbonisation projects.

Cluster 4 — Food and beverage

Nitrogen, CO₂ and oxygen are used for freezing, packaging, carbonation, modified-atmosphere packaging and cold-chain productivity.

Cluster 5 — Healthcare and life sciences

Medical oxygen, nitrous oxide, nitrogen and specialty medical gases remain critical public-health infrastructure. In a region exposed to demographic ageing and hospital modernisation, reliability matters.

Cluster 6 — Electronics, semiconductors and advanced manufacturing

Specialty gases and ultra-high-purity gases are required for chips, sensors, batteries, displays and precision production. This links industrial gases directly to Europe’s strategic technology agenda.

The result:

Industrial gases are not an input category. They are uptime, quality, safety, energy efficiency and strategic resilience.

4. 2026 CEE Market Reality

The CEE industrial gas market in 2026 is shaped by four tensions.

Tension 1 — Growth vs energy cost

CEE can grow through nearshoring, EU investment and industrial renewal, but high power and gas prices pressure margins. Industrial gas production is energy-intensive, especially air separation and hydrogen production.

Tension 2 — Customer demand vs affordability

Customers need reliable gases, but many energy-intensive customers face margin compression. Suppliers must help them reduce waste, optimize usage, and improve process productivity.

Tension 3 — Decarbonisation ambition vs hydrogen uncertainty

Hydrogen is strategically important, but early market design remains uncertain. A 2026 study of European hydrogen market design notes that only a small share of renewable hydrogen projects has reached final investment decision, partly because future hydrogen market design and operating rules remain uncertain.

Tension 4 — EU strategic autonomy vs dependency

Europe is trying to reduce dependency in raw materials, hydrogen, energy and technology. The EU Critical Raw Materials Act sets 2030 benchmarks: 10% of annual needs from extraction, 40% from processing, 25% from recycling, and no more than 65% dependency on a single third country at any relevant processing stage.

For CEE industrial gas players, these tensions create the opening for a new role:

From molecule seller to resilience partner.

5. The CEE Industrial Gas Flow Map

The Industrial Gas Explanation MASTER™ should map the region through strategic flows.

Flow 1 — Oxygen

Core for steel, metals, combustion, wastewater, healthcare and chemical processes.

Flow 2 — Nitrogen

Core for inerting, packaging, electronics, chemicals, safety, blanketing and food freezing.

Flow 3 — Argon

Core for welding, metallurgy, stainless steel, aluminum and high-quality industrial fabrication.

Flow 4 — Hydrogen

Core for refining, chemicals, future green steel, mobility pilots, energy storage and decarbonisation.

Flow 5 — CO₂

Core for food, beverage, dry ice, greenhouse enrichment, welding mixtures and selected chemical uses.

Flow 6 — Helium and specialty gases

Core for electronics, research, medical imaging, leak detection and advanced manufacturing.

Flow 7 — Energy input

Electricity and natural gas determine cost competitiveness. Industrial gas economics cannot be separated from the energy system.

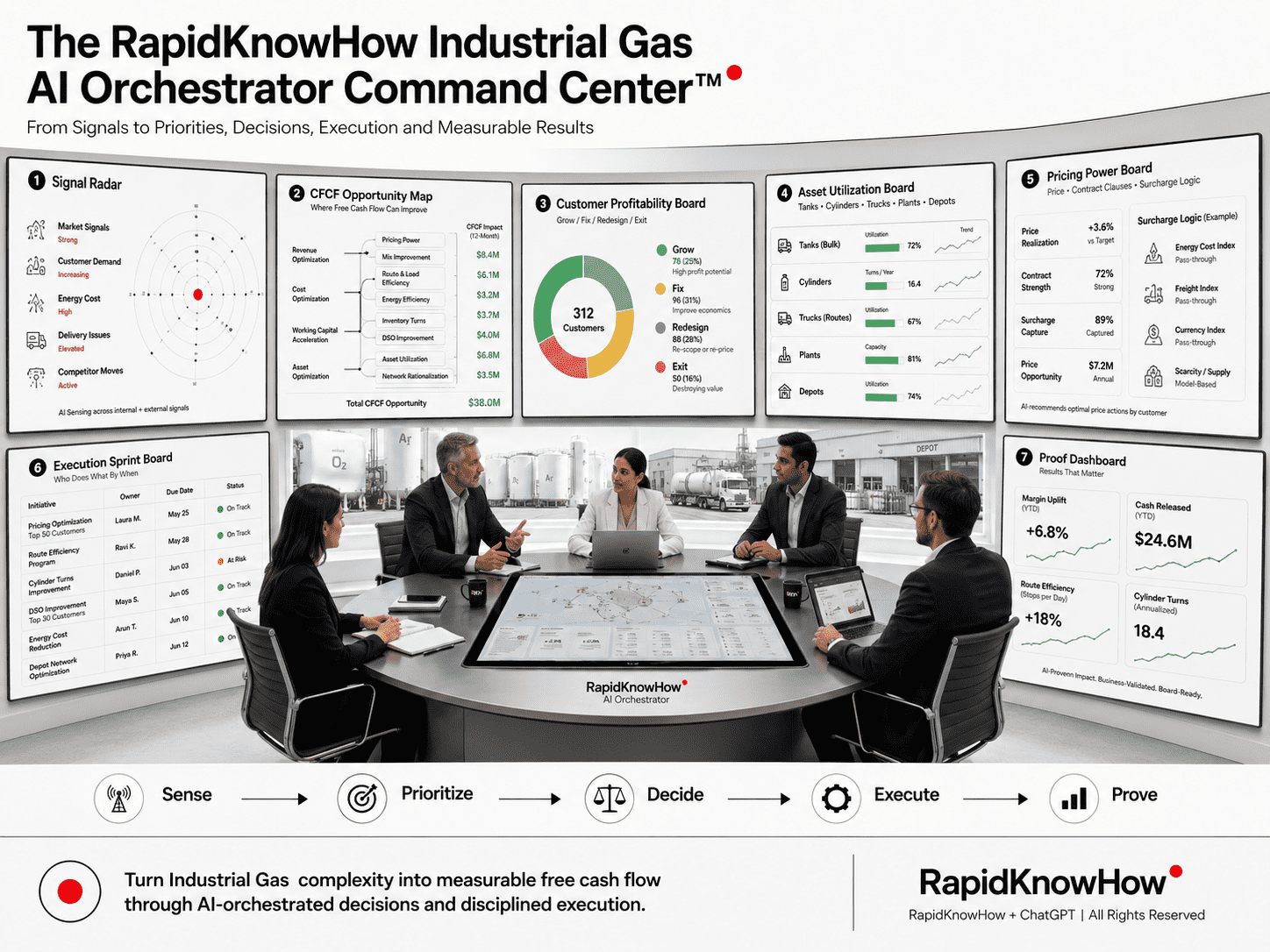

Flow 8 — Data and AI

Real-time demand sensing, predictive maintenance, customer usage analytics, routing optimization, contract margin control and ROCE dashboards will separate leaders from laggards.

6. CEE Priority Countries

Poland

The largest CEE industrial platform. Strong opportunity in hydrogen, refining, chemicals, food, steel, healthcare, and manufacturing. Poland is also connected to green hydrogen funding and industrial modernisation. Public reporting in 2026 indicates EU-backed hydrogen support in Poland, including major allocations for large-scale green hydrogen projects.

Czechia

Strong automotive, machinery, electronics and industrial base. OECD expects Czech growth of 1.9% in 2026 and 2.1% in 2027, with investment supported by EU funds, but risks from energy prices, Middle East disruption and trade restrictions.

Slovakia

Automotive-heavy and exposed to energy costs, inflation and weak confidence. OECD notes Slovak activity slowed in early 2026, while investment remains supported by EU funds and energy subsidies still shield many households.

Hungary

Important for automotive, batteries, electronics and manufacturing. Strategic opportunity exists in nitrogen, hydrogen, specialty gases, welding gases and industrial services, but political and EU-funding risks require careful contract discipline.

Romania

Growth opportunity in energy, infrastructure, healthcare, food, chemicals, metals and Black Sea logistics. Romania is strategically relevant for Ukraine support, Black Sea energy and Southeast European industrial development.

Bulgaria and Balkans

Selective opportunity in metals, food, healthcare, logistics, construction materials and energy transition. The region needs disciplined asset-light entry models and strong distributor/partner control.

7. Strategic Chokepoints for CEE Industrial Gas

There are ten CEE industrial-gas chokepoints:

- Electricity price and grid capacity

Air separation and hydrogen are power-sensitive. Low-carbon electricity access becomes a competitive weapon. - Hydrogen market design

Without clear offtake, certification and infrastructure rules, hydrogen investments risk delay. - Steel and metals transition

Oxygen, argon and hydrogen demand depend on whether regional metals plants modernize or decline. - Automotive transformation

EV, battery and electronics supply chains change demand from traditional fabrication toward specialty and high-purity gases. - Healthcare reliability

Medical gas infrastructure must be resilient and professionally managed. - CO₂ availability

Food and beverage customers need reliable CO₂, but supply can be disrupted when fertilizer, ammonia or ethanol plants reduce output. - Helium and specialty gas security

Advanced manufacturing and healthcare depend on scarce specialty gases. - Customer credit and contract risk

Energy-intensive customers may demand support but face margin stress. Contract quality matters. - Transport and logistics

Bulk liquid gases depend on depots, routing, driver availability and border/logistics resilience. - AI-orchestrated operating control

The winner will use AI dashboards to control demand, production, logistics, margin, energy exposure and customer risk in near-real time.

8. Strategic Opportunity: CEE Industrial Gas AI-Orchestrator™

The best 2026–2030 move is not to build blindly. It is to orchestrate.

The CEE Industrial Gas AI-Orchestrator™ should run five control loops:

1. Sense

Track customer demand, energy prices, plant utilization, logistics disruptions, CO₂ shortages, hydrogen projects and sector signals.

2. Prioritize

Rank customers by margin, strategic importance, credit risk, growth potential and resilience value.

3. Execute

Optimize supply mode: on-site, pipeline, bulk liquid, cylinder, distributor, partner, asset-light service or long-term offtake.

4. Improve

Reduce customer waste, improve yield, lower energy cost, improve safety, and capture measurable savings.

5. Scale

Convert best cases into repeatable PowerPosts, PowerReports, Action Guides, customer dashboards and license models.

This creates a clear commercial formula:

Industrial Gas Value = Secure Molecules × Customer Uptime × Energy Efficiency × Decarbonisation Impact × Contract Discipline

9. 2026–2030 Strategy

Strategy 1 — Protect the core cash-flow base

Focus on reliable oxygen, nitrogen, argon, CO₂ and medical gas supply for strong customers.

Strategy 2 — Build energy-price pass-through discipline

Do not absorb energy volatility silently. Create transparent indexation, surcharge logic and customer education.

Strategy 3 — Use hydrogen selectively

Avoid speculative hydrogen hype. Prioritize bankable offtake: refinery, ammonia, steel pilots, mobility hubs, industrial parks and EU-supported projects.

Strategy 4 — Create CEE sector dashboards

Build dashboards for steel, automotive, healthcare, food, electronics, chemicals and energy.

Strategy 5 — Develop asset-light partnerships

Use local distributors, engineering partners, service partners and digital customer tools before committing heavy capital.

Strategy 6 — Secure specialty gases

Protect helium and high-purity gas supply chains for advanced manufacturing, healthcare and laboratories.

Strategy 7 — Become the resilience partner

Sell not only gas, but customer uptime, safety, compliance, decarbonisation and measurable productivity improvement.

10. Final Strategic Result

CEE 2026 is not a passive industrial gas market. It is a live industrial resilience arena.

Energy volatility, war proximity, EU industrial policy, hydrogen uncertainty, critical raw-material dependency and customer margin pressure all converge in the region.

The winning industrial gas player will not be the one with the most cylinders or tanks alone.

The winner will be the one that controls the full value logic:

Sense demand. Secure molecules. Optimize energy. Protect customers. Improve processes. Capture margin. Scale resilience.

The RapidKnowHow conclusion is clear:

Industrial Gas in CEE 2026 means: not only supply gases — control strategic industrial flows. – Josef David