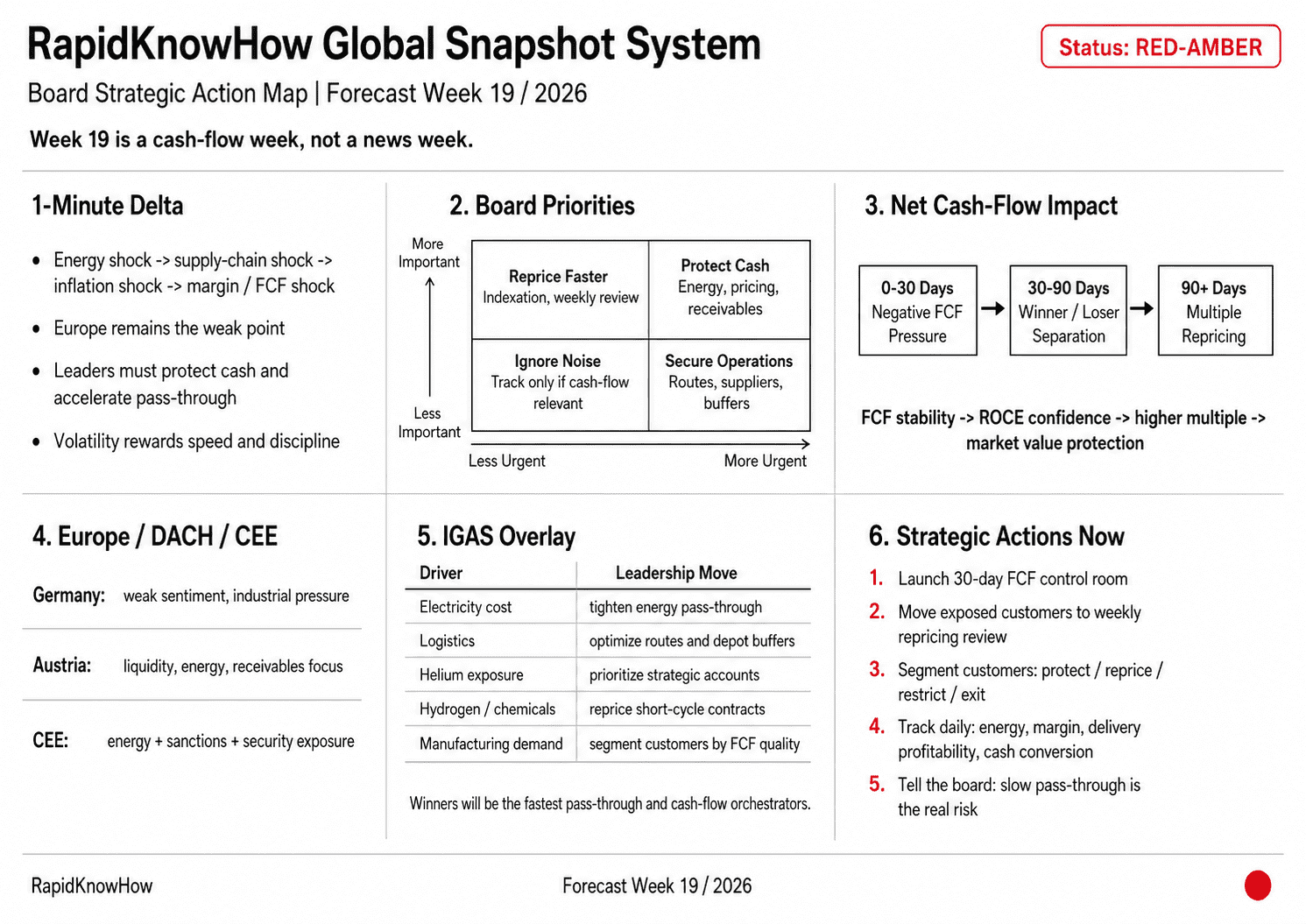

Forecast Status: RED-AMBER

Core Thesis: Week 19 will be dominated by the energy shock → supply-chain shock → inflation shock → margin/FCF shock sequence. The key management question is no longer “Will volatility continue?” but “Can leaders pass through cost, protect cash, and avoid margin leakage faster than competitors?”

A) 1-Minute Delta

The IMF baseline now sees global growth slowing to 3.1% in 2026 and 3.2% in 2027, assuming the Middle East conflict remains limited; downside risks dominate if the conflict broadens, trade tensions return, or financial markets reprice risk.

Europe is the weak point. The IMF says Europe is being hit by a new energy-driven supply shock, with euro area growth projected at only 1.1% in 2026.

The operational signal is now visible: eurozone PMI dropped below the 50 expansion line to 48.6, while input prices surged, showing a direct hit to production cost and margins.

B) Eisenhower Matrix — Week 19 Priorities

| Priority | Signal | RapidKnowHow Action |

|---|---|---|

| Urgent + Important | Energy shock, LNG/oil flow risk, TTF volatility | Activate 30-day cash-protection program |

| Important, not yet urgent | Customer pass-through, contract indexation, working capital | Reprice contracts, shorten review cycles |

| Urgent, less strategic | Freight delays, supplier bottlenecks | Secure alternatives, split routes, pre-book capacity |

| Noise | Daily political comments without supply impact | Track only if linked to price, volume, or sanctions |

Board sentence:

Week 19 is a cash-flow week, not a news week.

C) Net Cash-Flow Impact Lens

0–30 Days: Negative FCF Pressure

Expect pressure from higher energy, logistics, inventory buffers, and delayed customer pass-through. The IEA reports a historically severe oil supply disruption, with global oil supply falling sharply in March and crude benchmarks rising strongly after restrictions around the Strait of Hormuz.

30–90 Days: Winner/Loser Separation

Companies with automatic pass-through clauses, disciplined working-capital control, and AI-supported demand/supply forecasting should defend margins better. Laggards will absorb costs first, negotiate later, and lose FCF.

90+ Days: Multiple Repricing

The market will reward companies that convert volatility into visible FCF resilience. The formula remains:

FCF stability → ROCE confidence → higher multiple → market value protection.

D) Europe / DACH / CEE Focus

Germany

Germany is the clearest warning signal. The ifo Business Climate Index fell to 84.4 in April from 86.3 in March, the lowest level since May 2020. Ifo states that companies are more pessimistic, logistics are under pressure, chemicals are exposed, and construction sentiment has dropped sharply.

Austria

Austria is exposed through energy prices, industrial inputs, and transit/logistics pressure. For Austrian Mittelstand and industrial suppliers, the Week 19 focus should be liquidity, energy contracts, receivables, and customer repricing.

CEE

CEE faces a dual squeeze: energy exposure plus proximity to Ukraine/Russia risk. The EU’s 20th sanctions package against Russia, adopted on 23 April, targets energy revenues, military-industrial supply chains, trade, financial services, and crypto-linked channels.

E) Industrial Gas Deep-Dive Overlay

IGAS Week 19 Risk Level: HIGH but manageable for leaders

Industrial gases are directly exposed through:

| IGAS Driver | Week 19 Impact | Leadership Move |

|---|---|---|

| Electricity cost | Margin pressure in ASUs | Tighten energy pass-through |

| Logistics | Bulk delivery cost rises | Route optimization + depot buffers |

| Helium | Semiconductor / high-tech risk | Prioritize strategic accounts |

| Hydrogen / chemicals | Input and feedstock volatility | Reprice short-cycle contracts |

| Healthcare oxygen | Defensive demand | Protect service reliability |

| Metals / manufacturing | Volume risk | Segment customers by FCF quality |

The ECB warned that prolonged disruption can move from price pressure to real shortages, noting that Gulf-linked inputs such as helium, fertilizers, and methanol are exposed, with implications for semiconductors, food prices, chemicals, and plastics.

IGAS CEO sentence:

The winners will not be the biggest gas companies; the winners will be the fastest pass-through and cash-flow orchestrators.

Linde will release Q1 2026 results on 1 May, immediately before Week 19, while Air Liquide presents Q1 revenue on 28 April; their management commentary will become a key sector signal for pricing power, energy exposure, and demand resilience.

F) Red-Flag Alerts for Week 19

| Red Flag | Trigger | FCF Meaning |

|---|---|---|

| Hormuz disruption persists | Oil/LNG flow instability | Energy surcharge acceleration |

| TTF gas > €50/MWh | Europe energy stress | Margin compression risk |

| Eurozone PMI remains <50 | Weak activity | Volume + pricing pressure |

| German ifo falls again | DACH recession signal | Capex delay, receivable risk |

| Ukraine escalation / sanctions retaliation | Security shock | CEE supply and credit risk |

G) Week 19 Strategic Action Proposal

1. Protect Cash First

Launch a 30-day FCF control room: receivables, overdue payments, inventories, energy surcharges, freight premiums.

2. Reprice Faster

Move from quarterly to weekly cost-pass-through review for exposed customers.

3. Segment Customers

Separate customers into: protect, reprice, restrict, exit.

4. Use AI-Orchestrator Logic

Track daily: energy price, logistics delay, customer margin, delivery profitability, cash conversion.

5. Prepare the Board Message

“Volatility is not the problem. Slow pass-through is the problem.”

H) Final RapidKnowHow Forecast

Week 19/2026 will be a stress-test week for Europe, DACH, and industrial companies.

The companies that defend FCF, ROCE, and pricing discipline will strengthen. The companies that wait for “normalization” will lose margin, cash, and strategic freedom.

RapidKnowHow Forecast:

RED-AMBER → Cash-Flow Defense + Pass-Through Acceleration + AI-Orchestrated Control. – Josef David